Skip to main content

Skip to footer

Deutsch

Login

Prospective Students

Students

Researchers

HIS/LSF

Groupware

Accounts

Telephone Directory

Media

International Office

Search

Submit

Search

Quick Access

Faculty of Law and Economics

Menu

Search

Target Groups

Study

Research

Chairs

Staff

Faculty

Faculty of Law and Economics

Chairs

General Business Administration

Chair of Business Administration and Finance

E-learning

E-exploring

Quantitative Finance

E-exploring

E-exploring

Quantitative Finance

Risk Management

Quantitative Finance

American Call and Put Option

Asset Allocation

Basic Option Trading Strategies

Binary Options Pricing and Greeks

Binomial Tree

Bond Pricing

Brownian Bridge

Chooser Options

Early Excercise of American Options

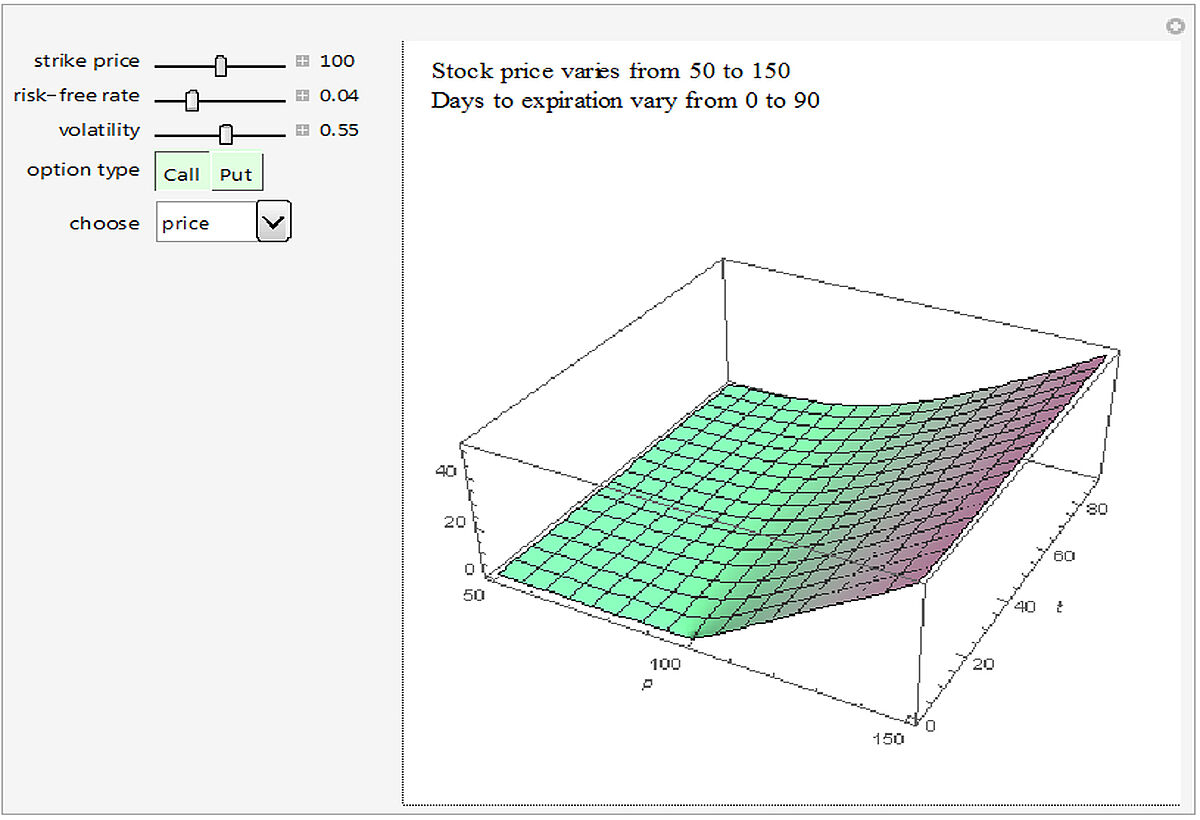

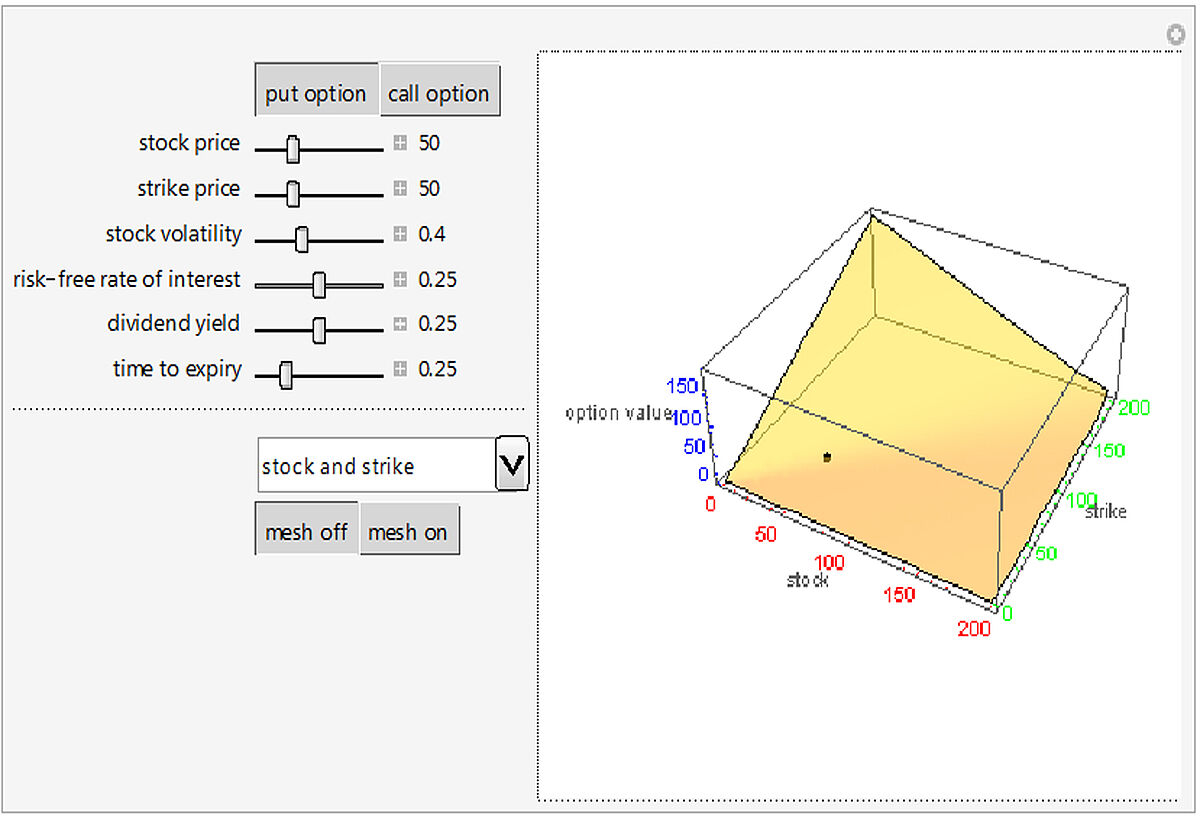

European Option Prices and Greeks in 3D

Expected Returns of the Dow - Industrials Beta Model

Expected Returns of the Dow - Industrials Fama French Model

Expected Utility Optimal Asset Investment

Expected Utility Optimal Insurance

Exploring the Black Scholes Formula

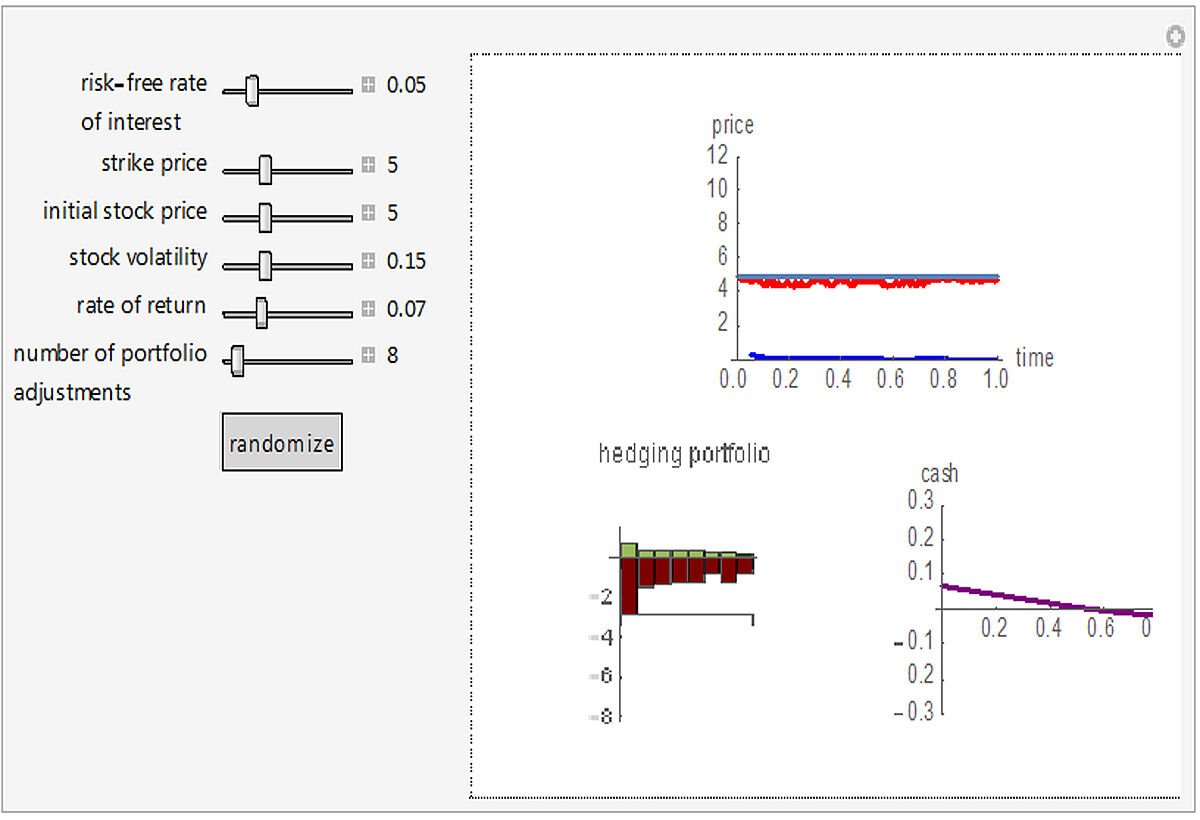

Hedging the Black Scholes Call Option

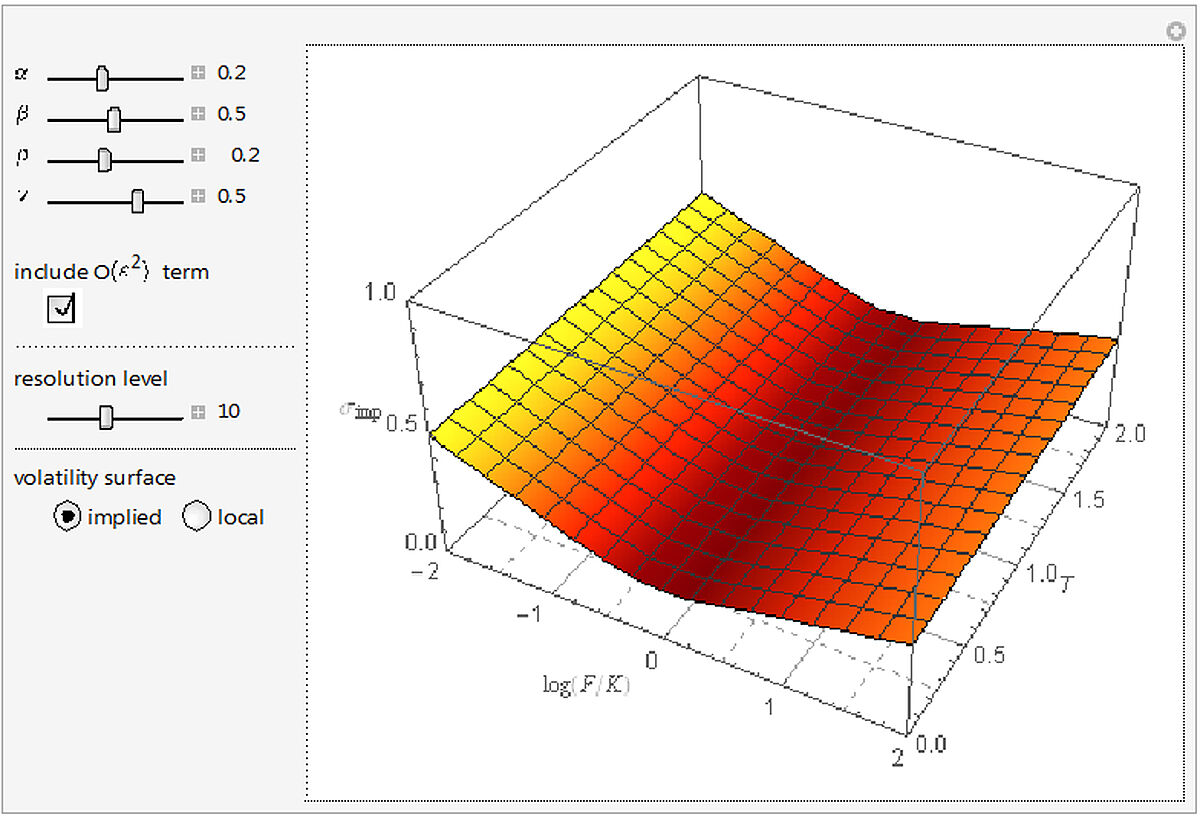

Implied and Local Volatility Dynamics in the SABR Model

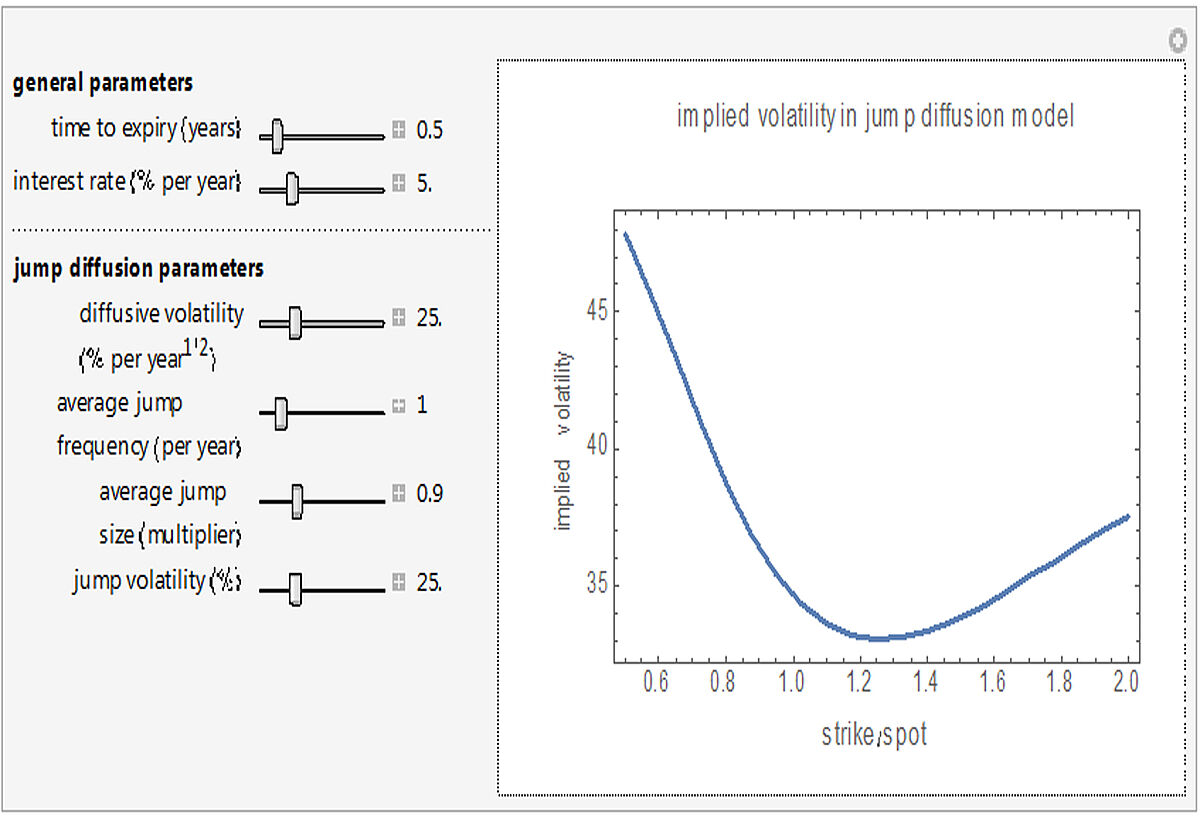

Implied Volatility in Merton's Jump Diffusion Model

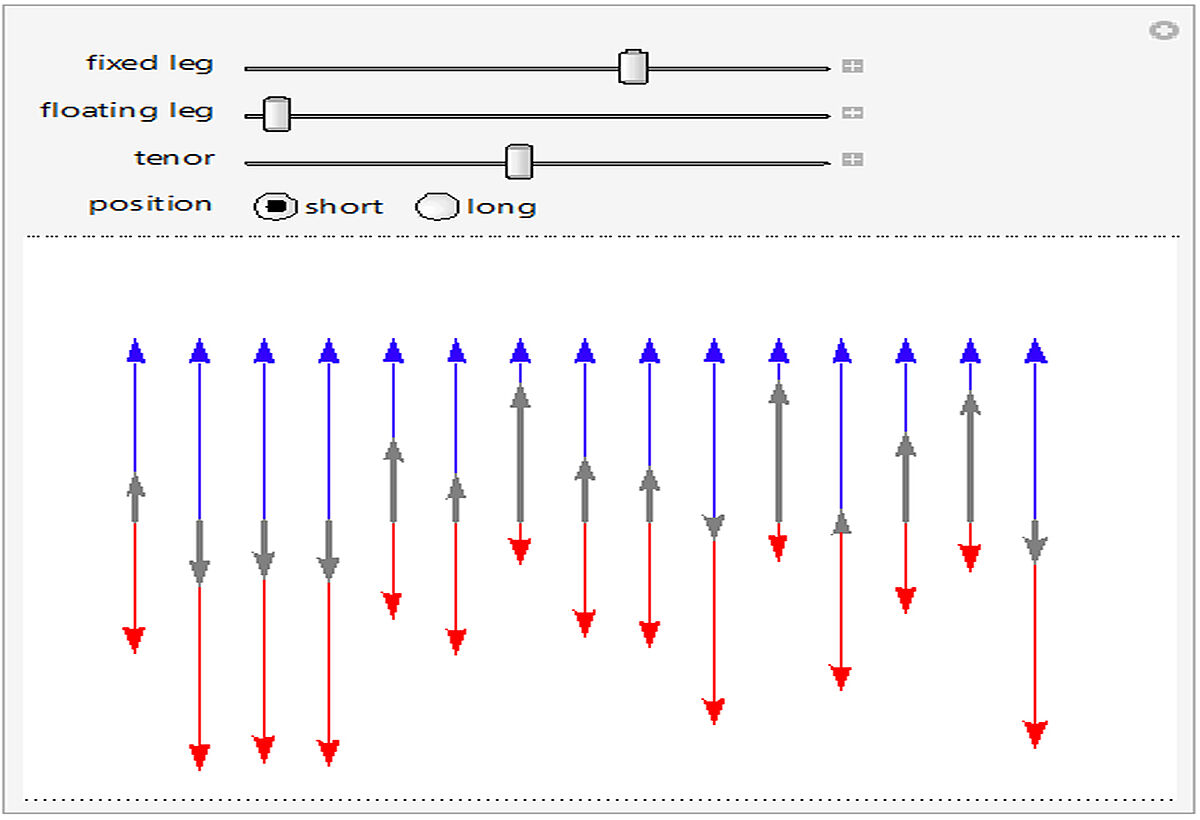

Interest Rate Swap

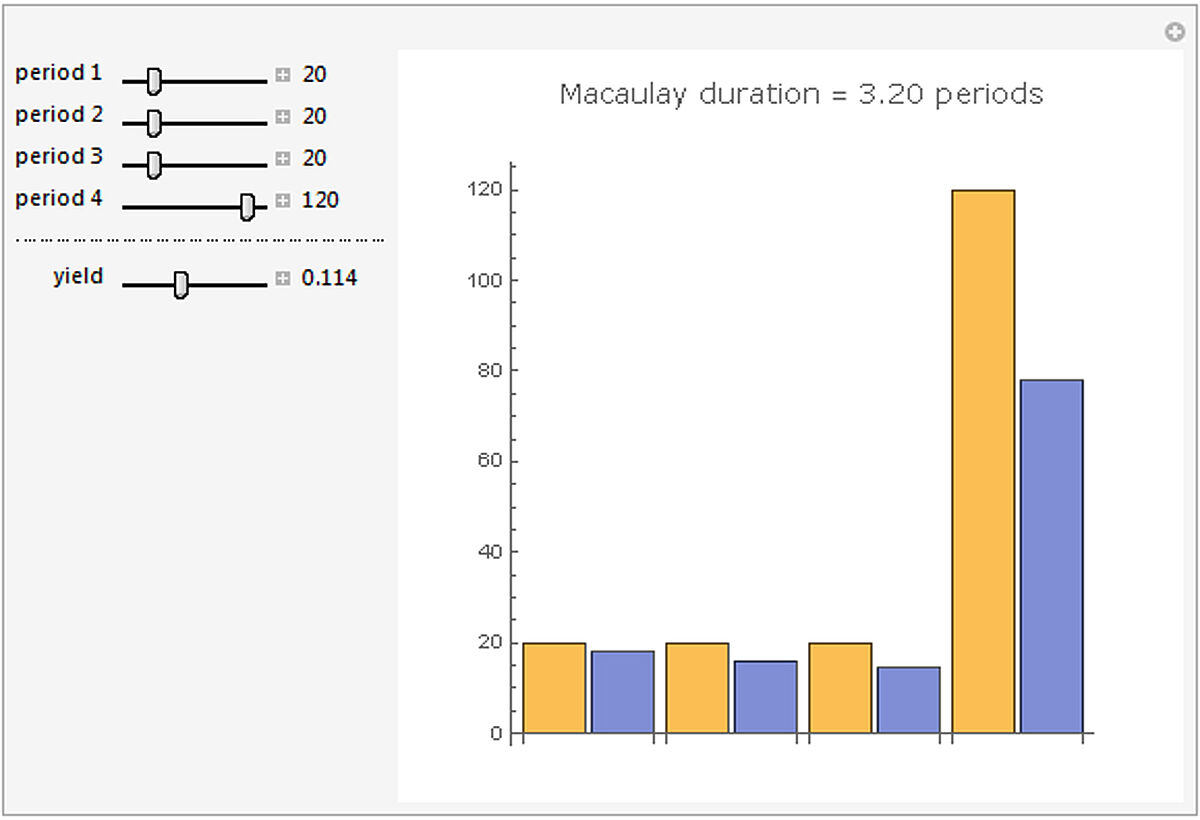

Macauly Duration

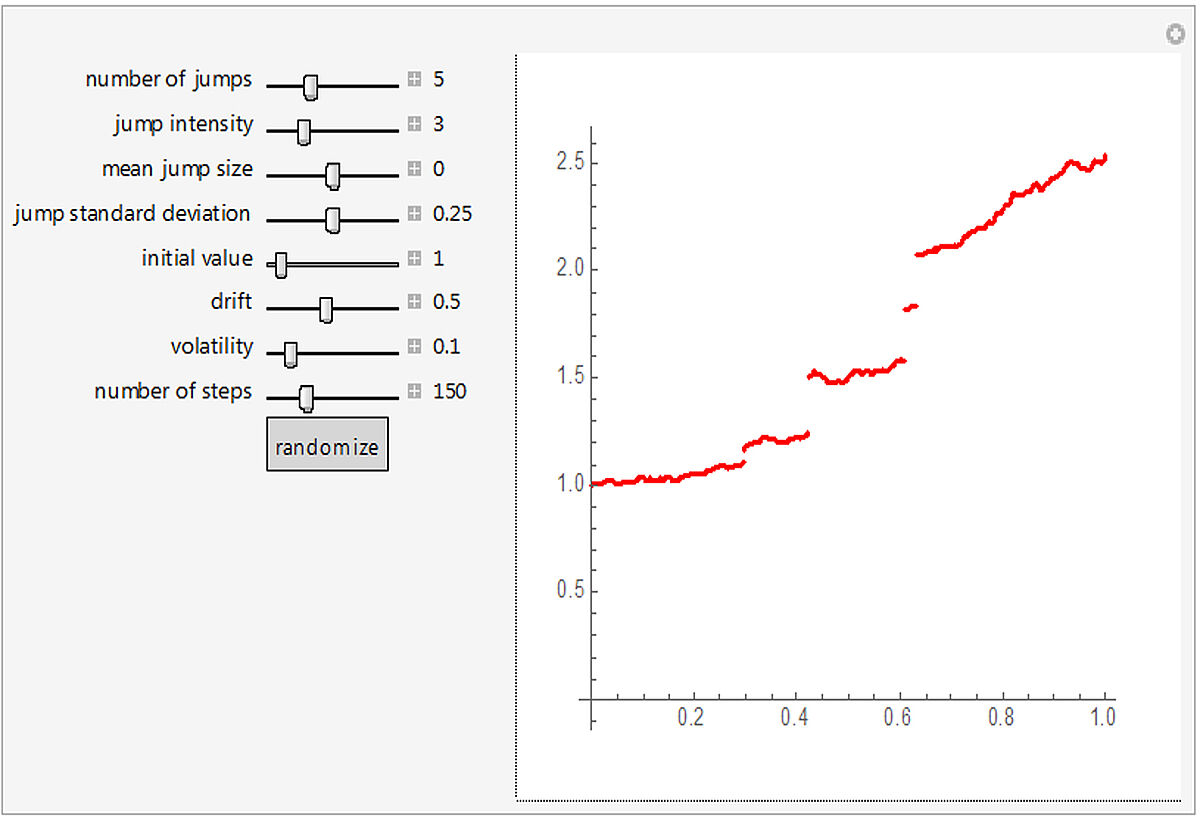

Merton's Jump Diffusion Model

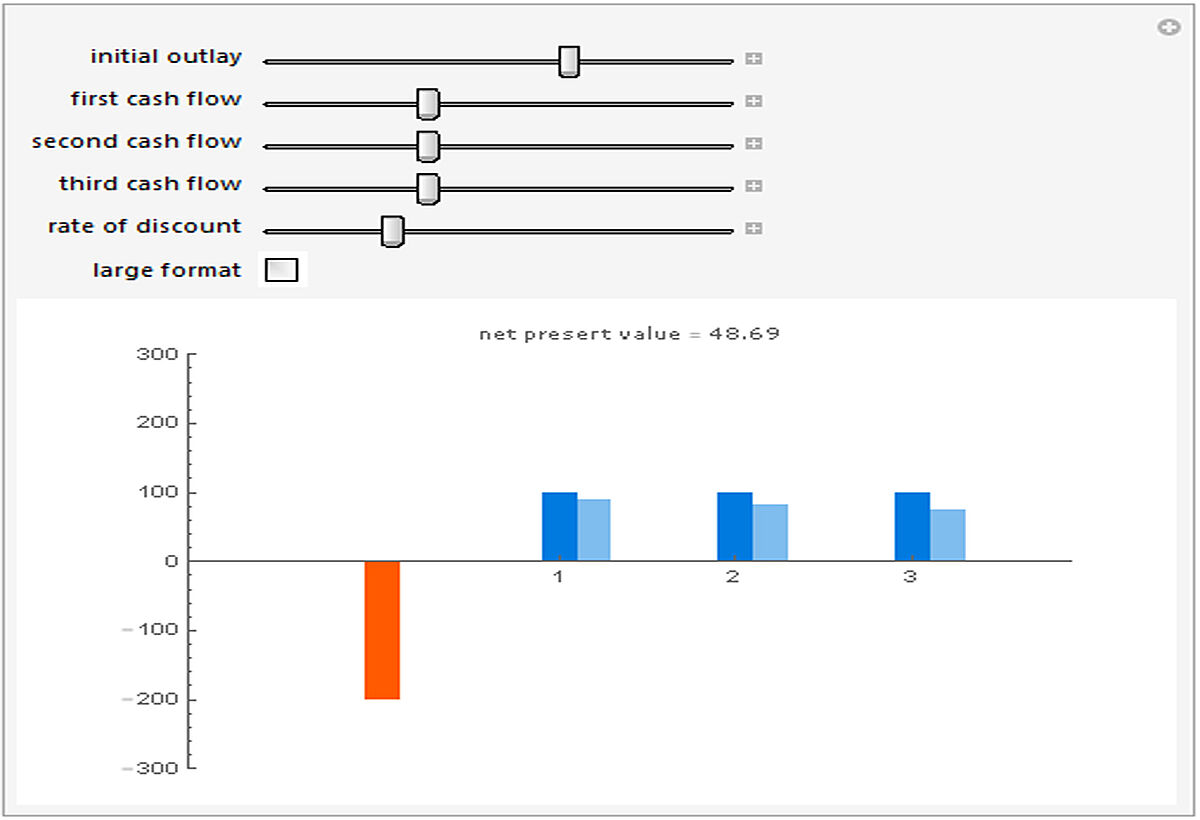

Net Present Value

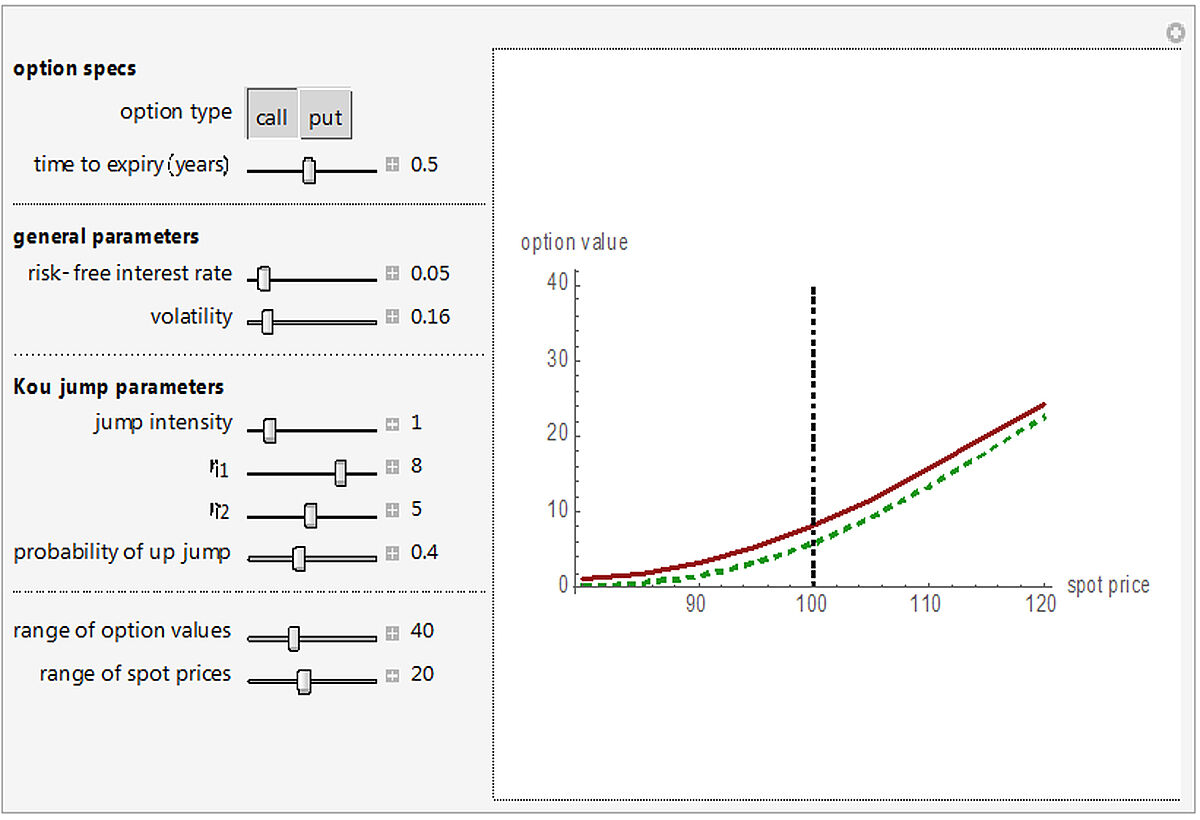

Option Prices in the Kou Jump Diffusion Model

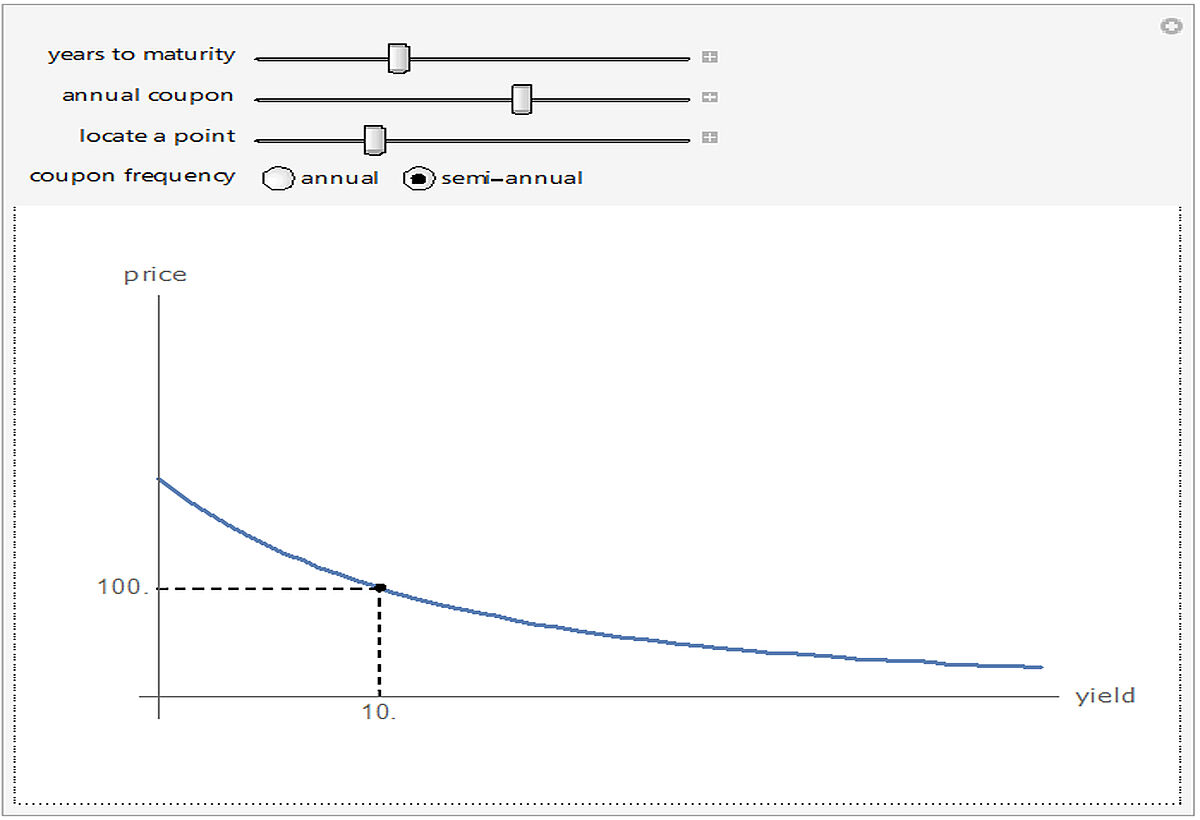

Price-Yield-Curve

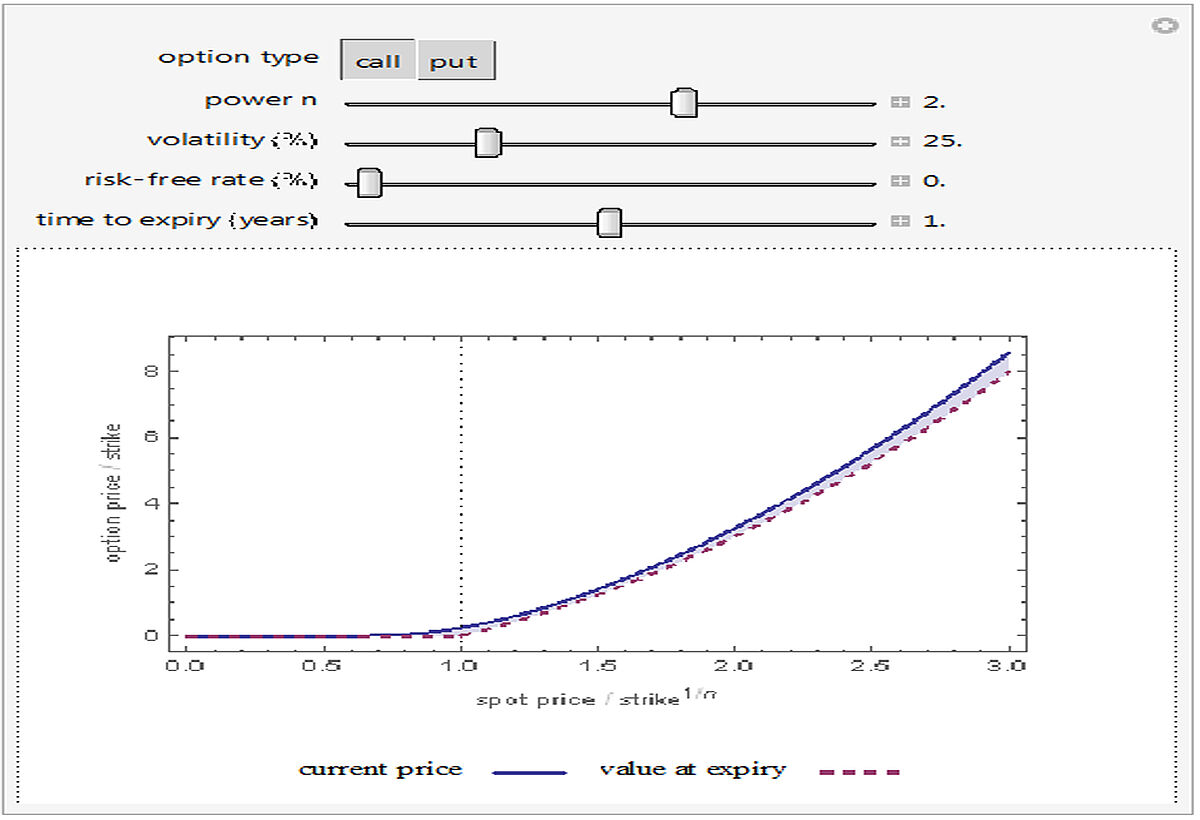

Pricing Power Options in the Black Scholes Model

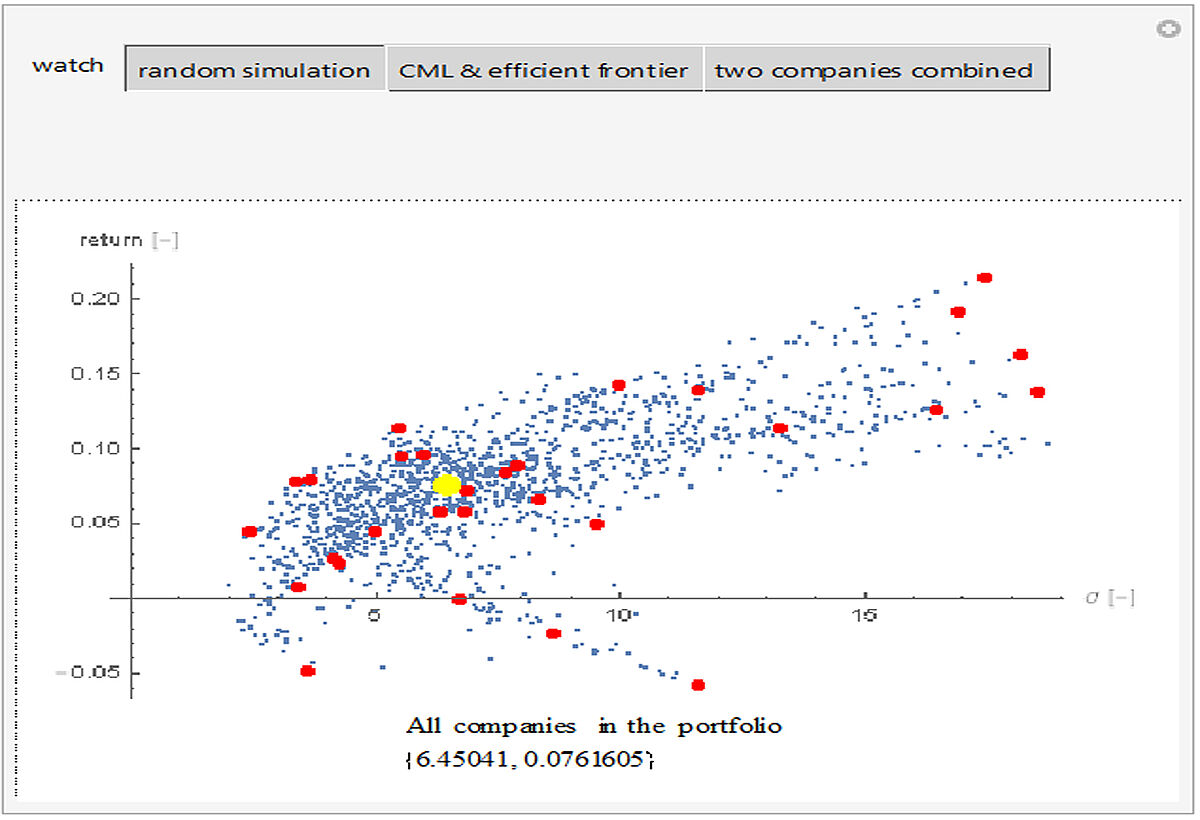

Random Simulation of a Financial Portfolio

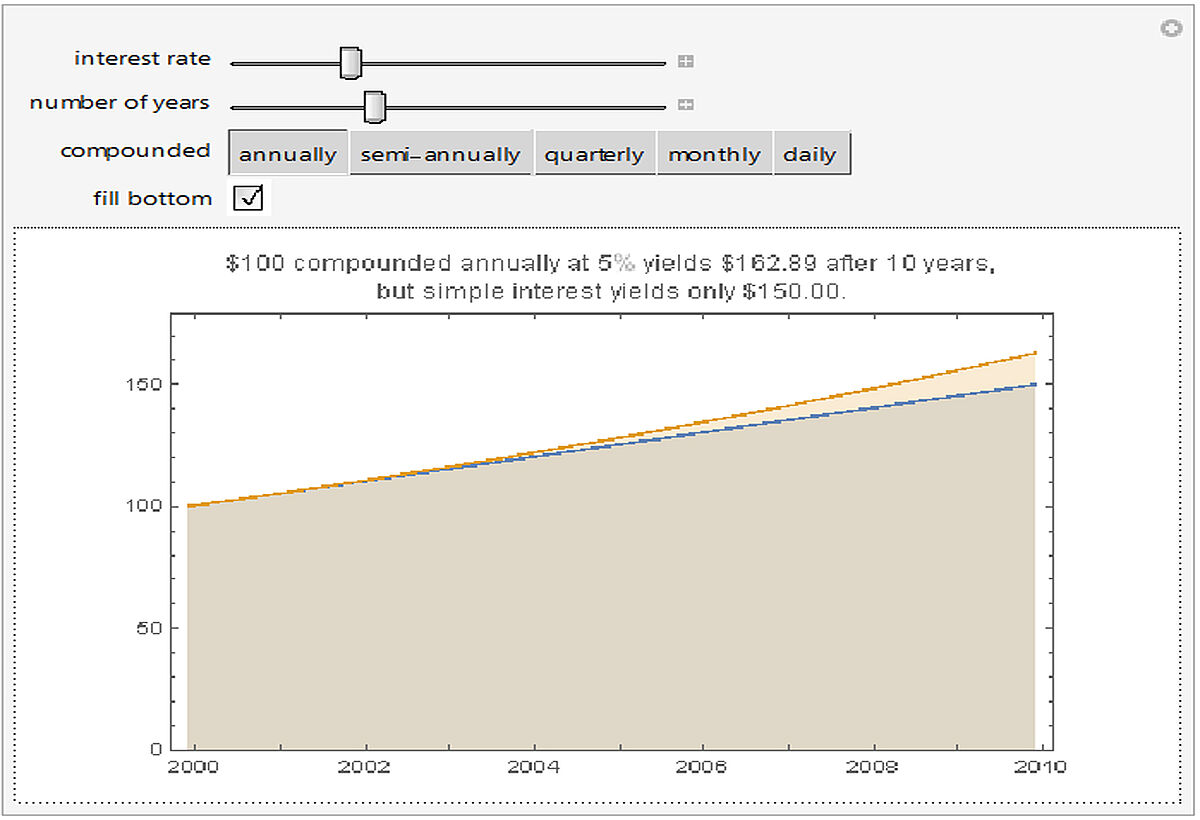

Simple versus Compound Interest

Term Structure of Interest Rates

The Itô Integral and Itô's Lemma

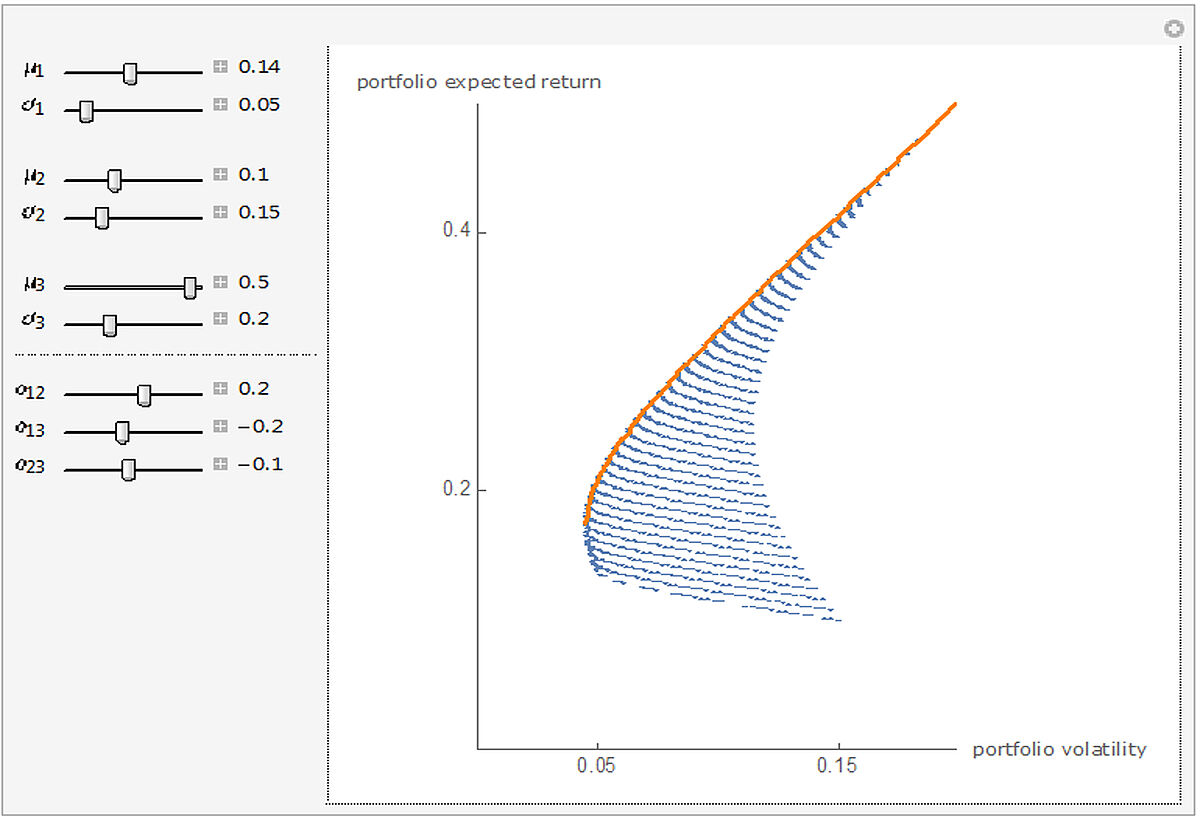

Three Asset Efficient Frontier

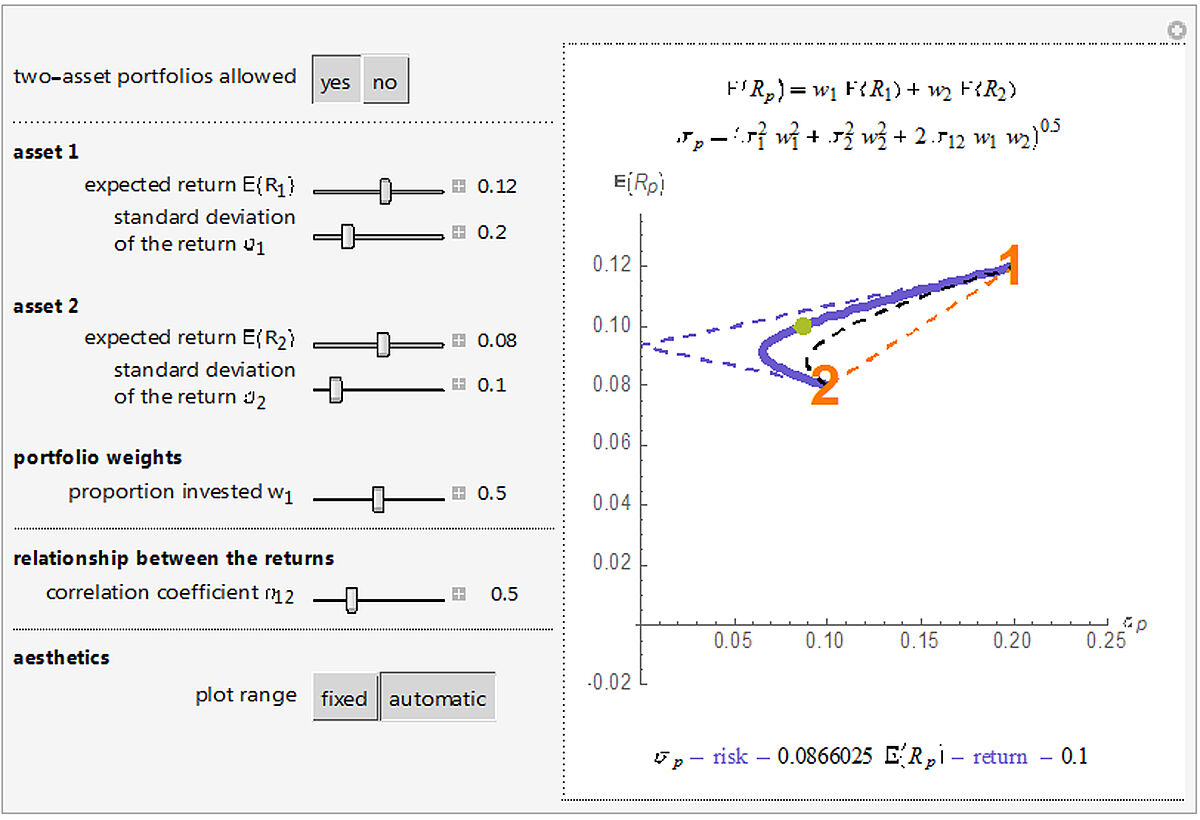

Two Asset Markowitz Feasible Set

Volatility Surface in the Heston Model

Yield Spot and Forward Curves

back to top