Zum Hauptinhalt

Zum Footer

English

Anmelden

Studieninteressierte

Studierende

Forschende

Internationale

HIS/LSF

Groupware

Accounts

Satzungen

Medien

Förderer

Alumni

Telefonsuche

Verwaltung

Universitätsmedizin

Konfliktmanagement

Suche

Absenden

Suche

Wegweiser

Rechts- und Staatswissenschaftliche Fakultät

Menü

Suche

Wegweiser

Studium

Studienangebot und Einschreibung

Rechtswissenschaften studieren

Rechtswissenschaften (Staatsexamen)

Bachelor-Teilstudiengang Öffentliches Recht (B.A.)

Bachelor-Teilstudiengang Privatrecht (auslaufend)

Öffentliches Recht im Nebenfach

Wirtschaftswissenschaften studieren

Bachelor BWL (B.Sc.)

Bachelor Management und Recht (B.Sc.)

Bachelor-Teilstudiengang BWL (B.A.)

Bachelor-Teilstudiengang VWL (B.A.)

Master BWL (M.Sc.)

Master Health Care Management (M.Sc.)

Diplom BWL (auslaufend)

Informationen rund um das Studium

Informationen für Erstsemester

Vorlesungsverzeichnisse

HIS (Kurseinschreibung)

Moodle (Lernplattform)

Studien- und Prüfungsordnungen

Bekanntmachungen und Hinweise

Schlüsselkompetenzen - Englisch, Kommunikationstechniken, Rhetorik, Mathematik

Internationales Studium

Studienangebot und weitere Informationen

Studienangebot und Bewerbung

Wirtschaft in Greifswald studieren

Fachstudienberatung

Studiendekan

Fachschaften

Praktikumsbörse

Berufsberatung

Forschung

Zur Startseite der Fakultät

Forschungsschwerpunkte

Forschungsschwerpunkte der Fakultät (Übersicht)

Institut für Energie-, Umwelt- und Seerecht (IfEUS)

Institut für Klimaschutz, Energie und Mobilität (IKEM)

Veröffentlichungen, Projekte

Veröffentlichungen

Forschungsprojekte

Vortragsreihen

Diskussionspapiere Wirtschaftswissenschaften

Promotion

Informationen für Promotions-Anwärter/innen

Abgeschlossene Promotionen

Habilitation

Habilitationsordnung

Abgeschlossene Habilitationen

Lehrstühle

Übersicht der Lehrstühle an der Fakultät

Rechtswissenschaften

Bürgerliches Recht

Strafrecht

Öffentliches Recht

Wirtschaftswissenschaften

Allgemeine Betriebswirtschaftslehre

Allgemeine Volkswirtschaftslehre

Personal

Zur Startseite der Fakultät

Professorinnen und Professoren

Professoren Rechtswissenschaften

Professoren Wirtschaftswissenschaften

Honorarprofessoren

Professoren im Ruhestand

Ehemalige Professoren

Dozentinnen und Dozenten

Lehrkräfte für besondere Aufgaben

Lehrbeauftragte

Privatdozenten

Vertretungen

Alphabetische Verzeichnisse

Mitarbeitende A-Z

Professoren A-Z

Fakultät

Zur Startseite der Fakultät

Dekanat

Aktuelles

Fakultätsleitung

Dekanatsbüro

Zeugnisübergabe

Stellenausschreibungen

Notfallpläne

Wo Sie uns finden

Kontakt

Gremien und Beauftragte

Fakultätsrat

Prüfungsausschüsse

Gleichstellungsbeauftragte

Fachschaften

Einrichtungen

Fachbibliothek

EDV-Abteilung

Geschichte und Gegenwart

Geschichte der Fakultät

Verein zur Förderung der Wirtschaftswissenschaften

Ereignisse und Meldungen (Archiv)

Bilderbuch

Jura & WiWi

Lehrstühle

Wirtschaftswissenschaften

Allgemeine Betriebswirtschaftslehre

Lehrstuhl für ABWL und Finanzwirtschaft, insbesondere Unternehmensbewertung

E-Learning

E-Exploring

Quantitative Finance

E-Exploring

E-Exploring

Quantitative Finance

Risikomanagement

Quantitative Finance

American Call and Put Option

Asset Allocation

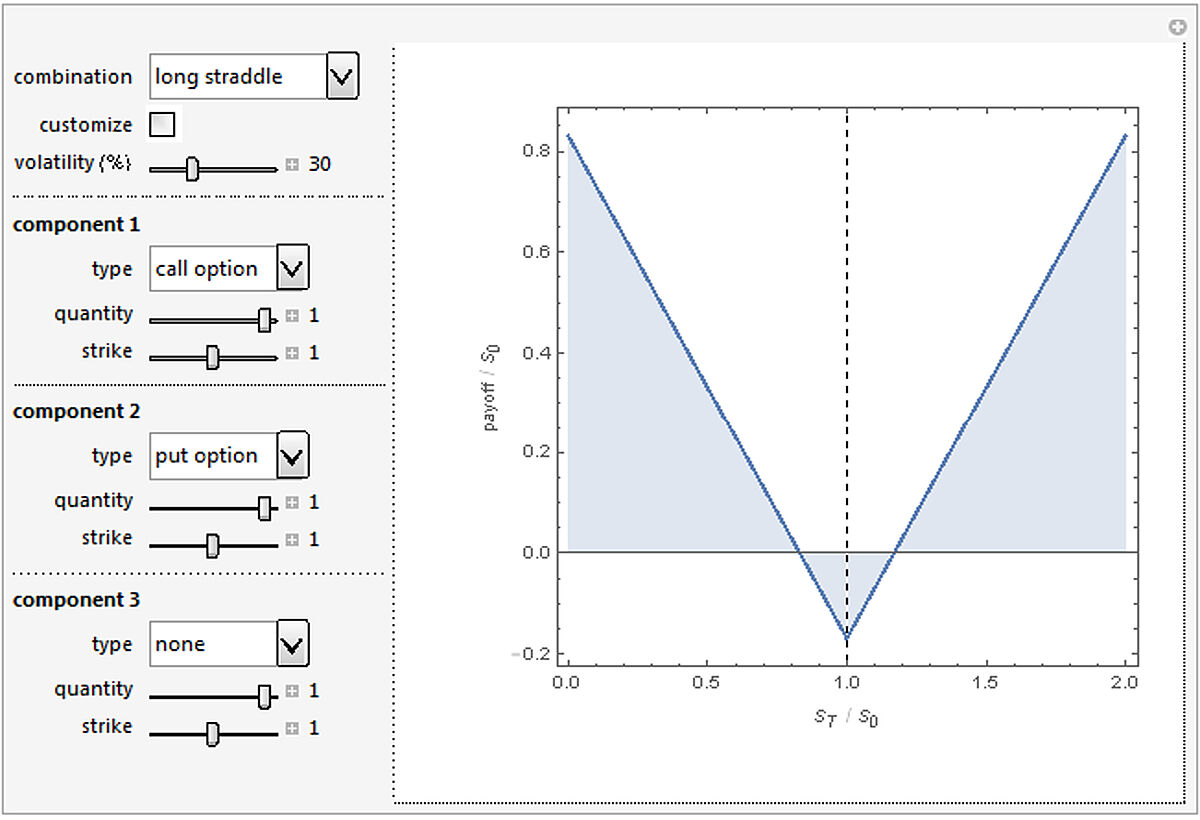

Basic Option Trading Strategies

Binary Options Pricing and Greeks

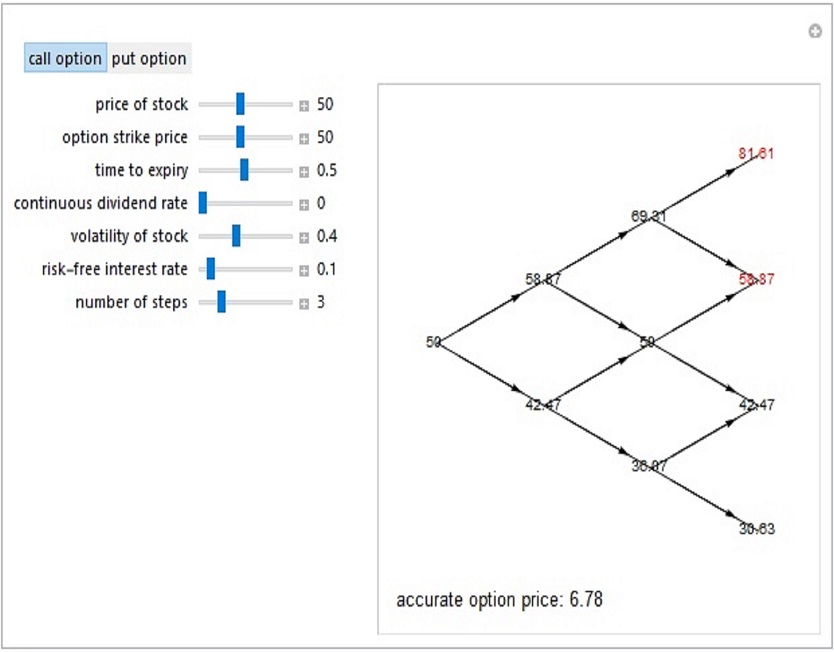

Binomial Tree

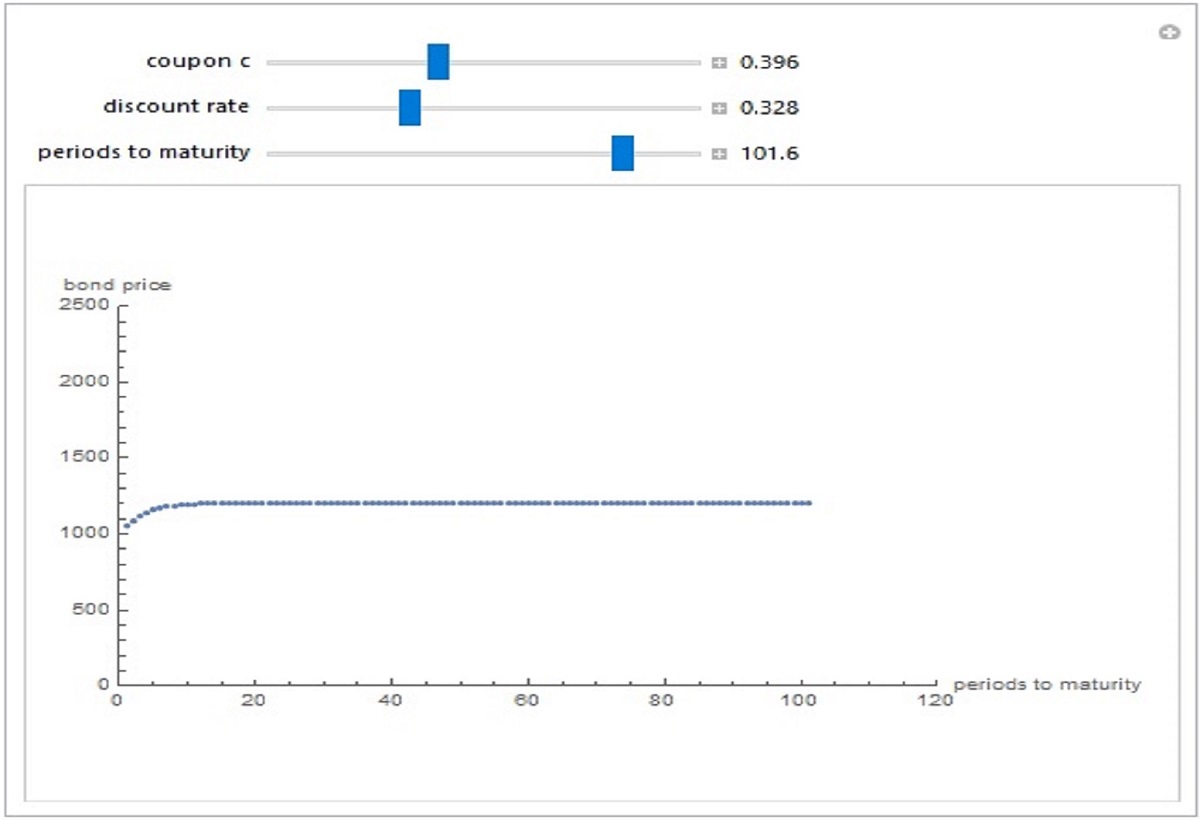

Bond Pricing

Brownian Bridge

Chooser Options

Early Excercise of American Options

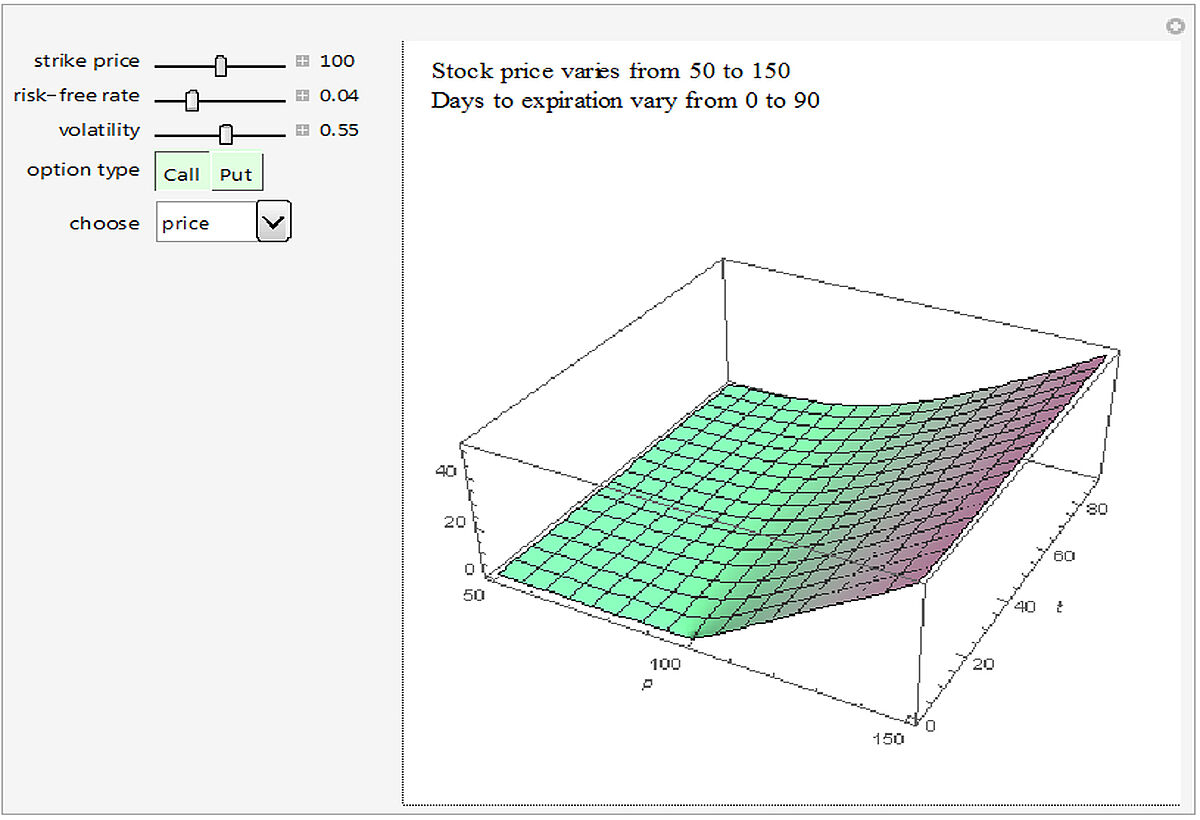

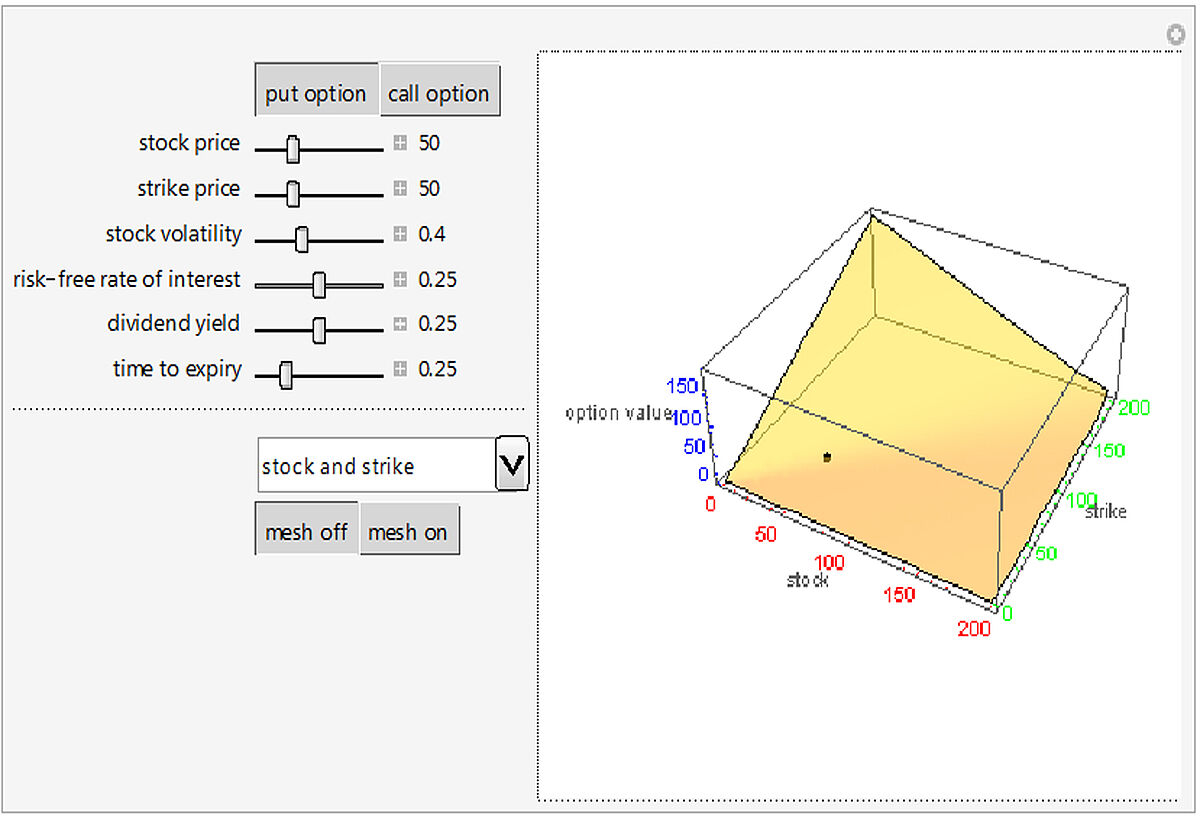

European Option Prices and Greeks in 3D

Expected Returns of the Dow - Industrials Beta Model

Expected Returns of the Dow - Industrials Fama French Model

Expected Utility Optimal Asset Investment

Expected Utility Optimal Insurance

Exploring the Black Scholes Formula

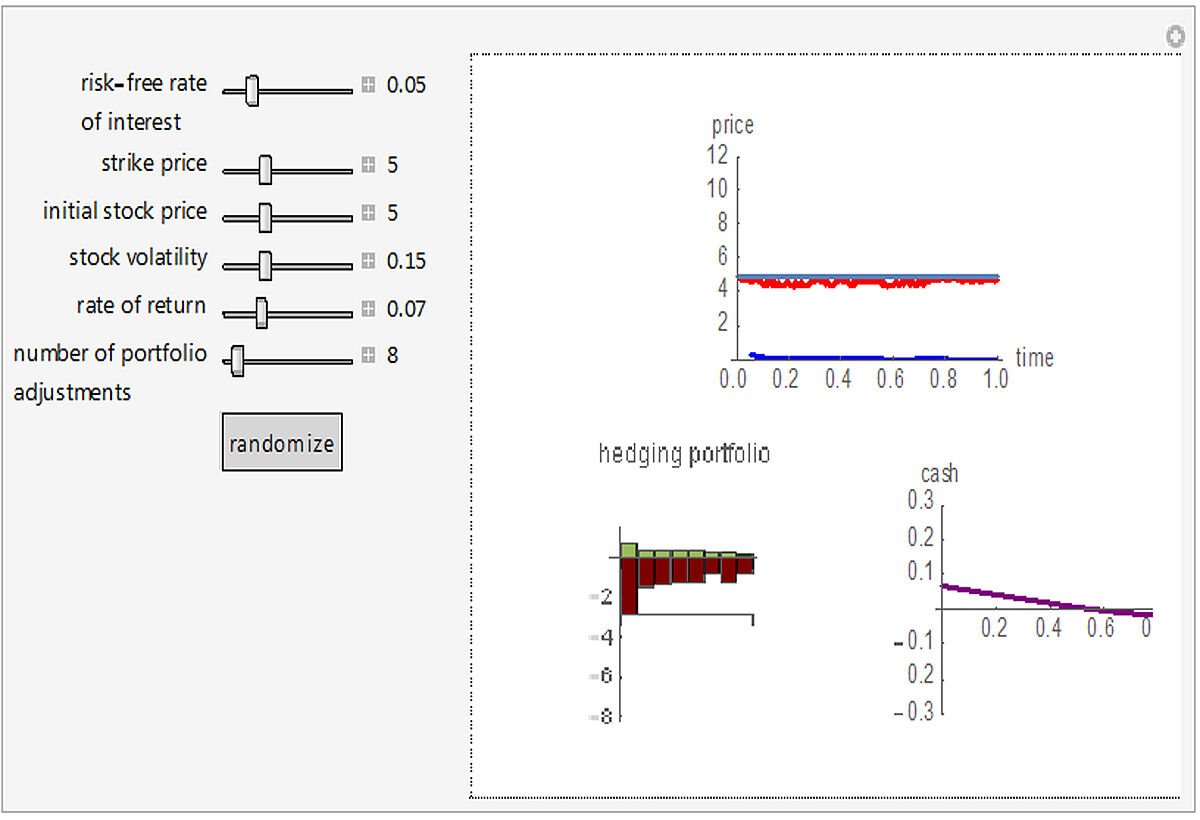

Hedging the Black Scholes Call Option

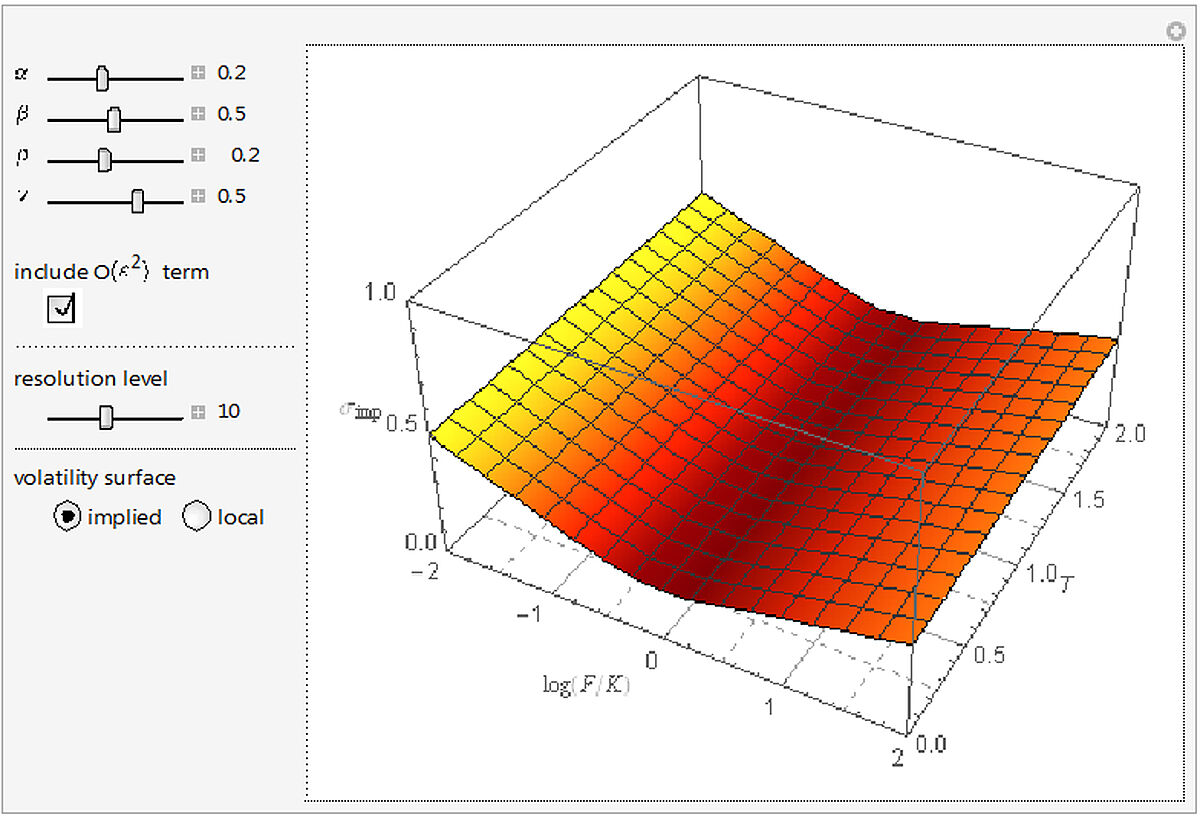

Implied and Local Volatility Dynamics in the SABR Model

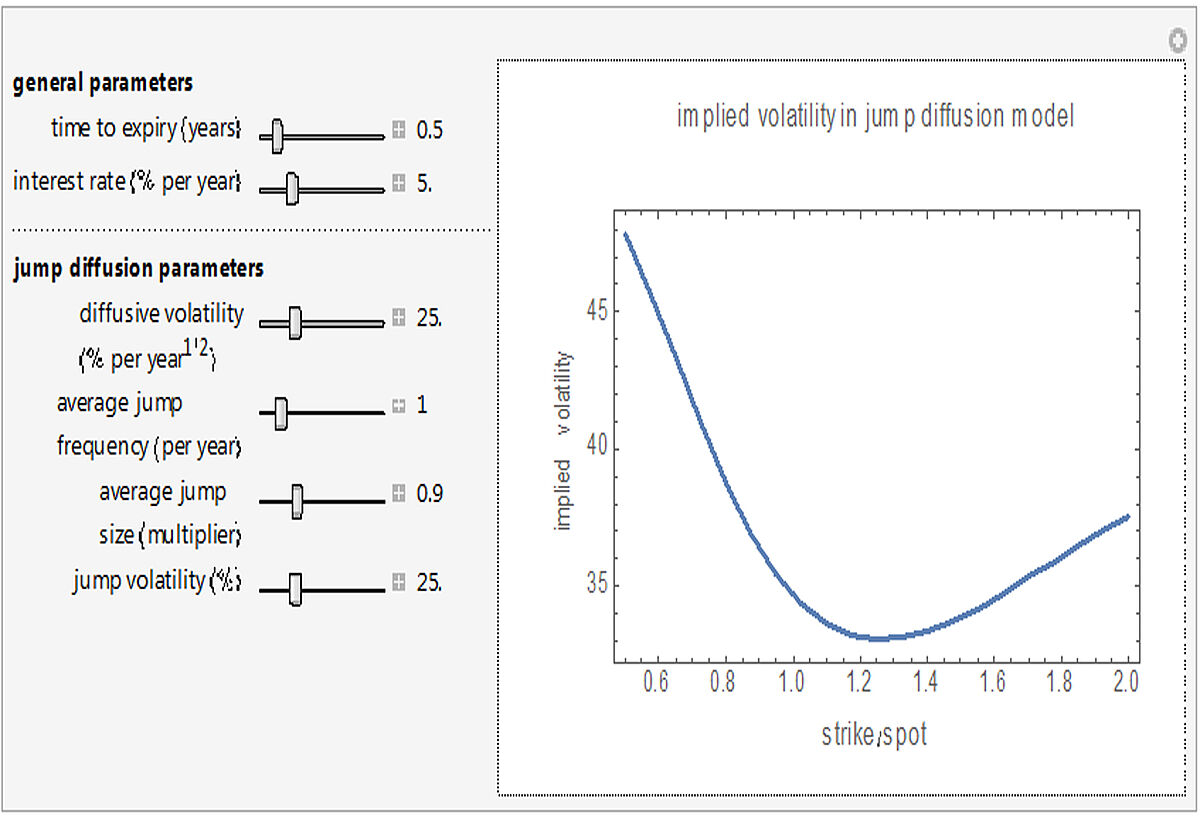

Implied Volatility in Merton's Jump Diffusion Model

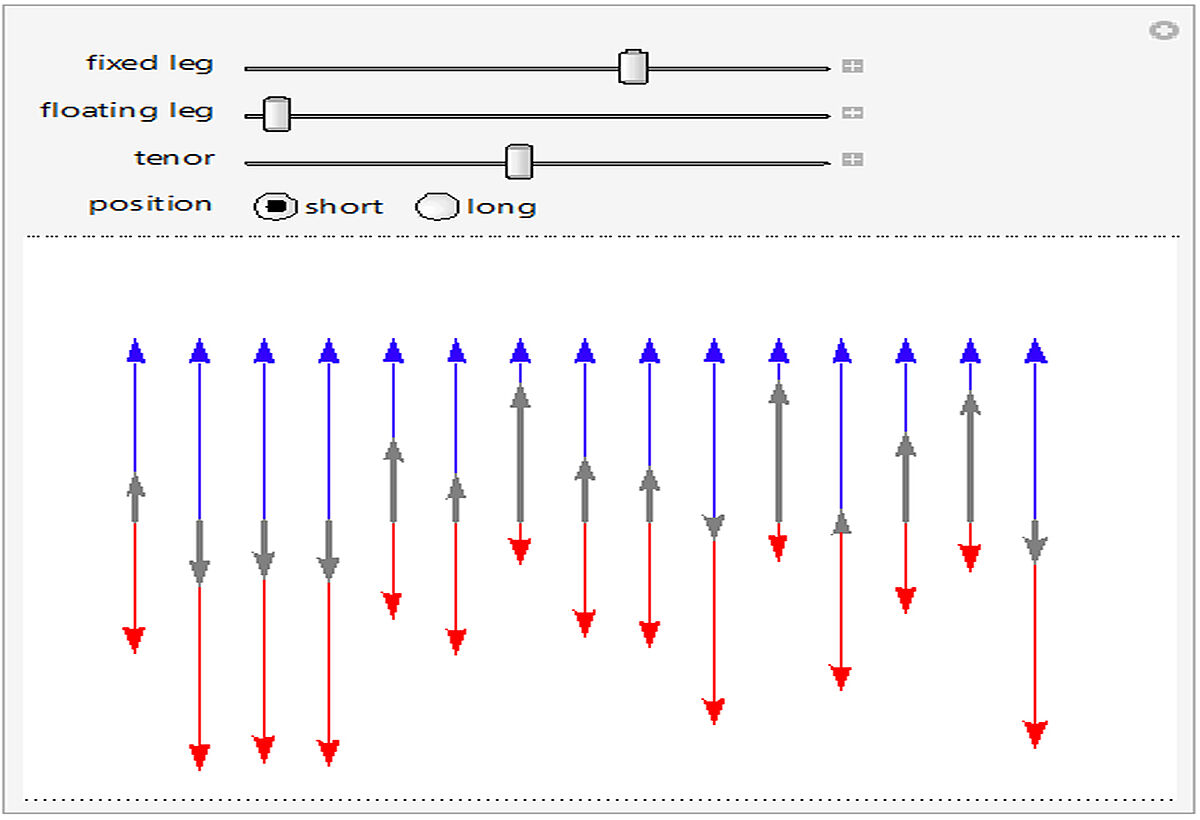

Interest Rate Swap

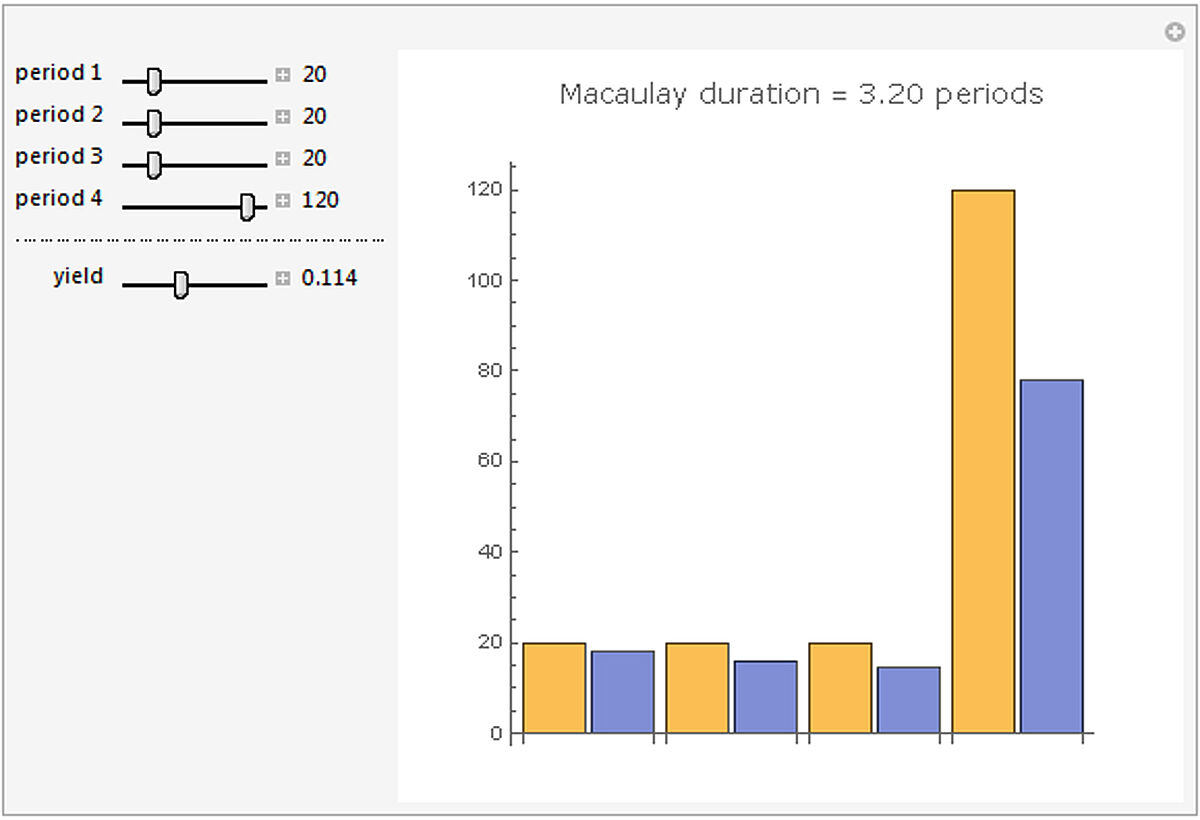

Macauly Duration

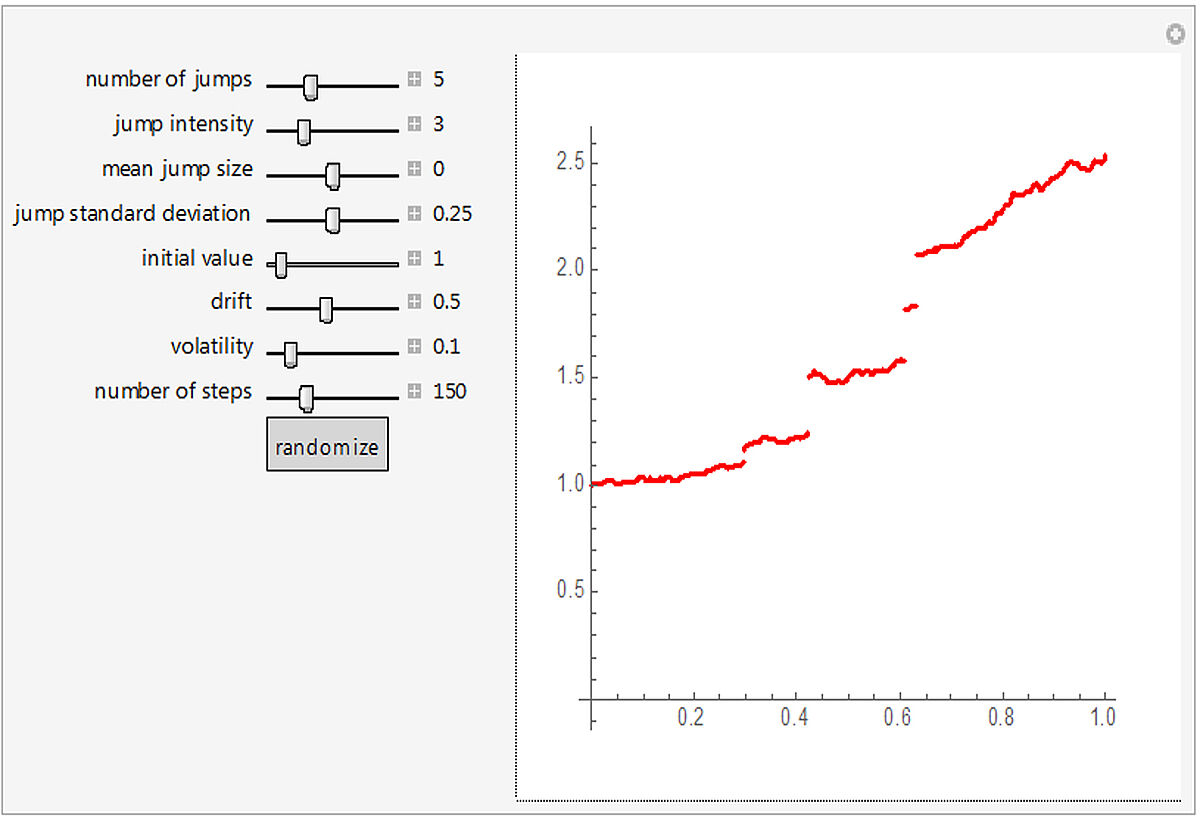

Merton's Jump Diffusion Model

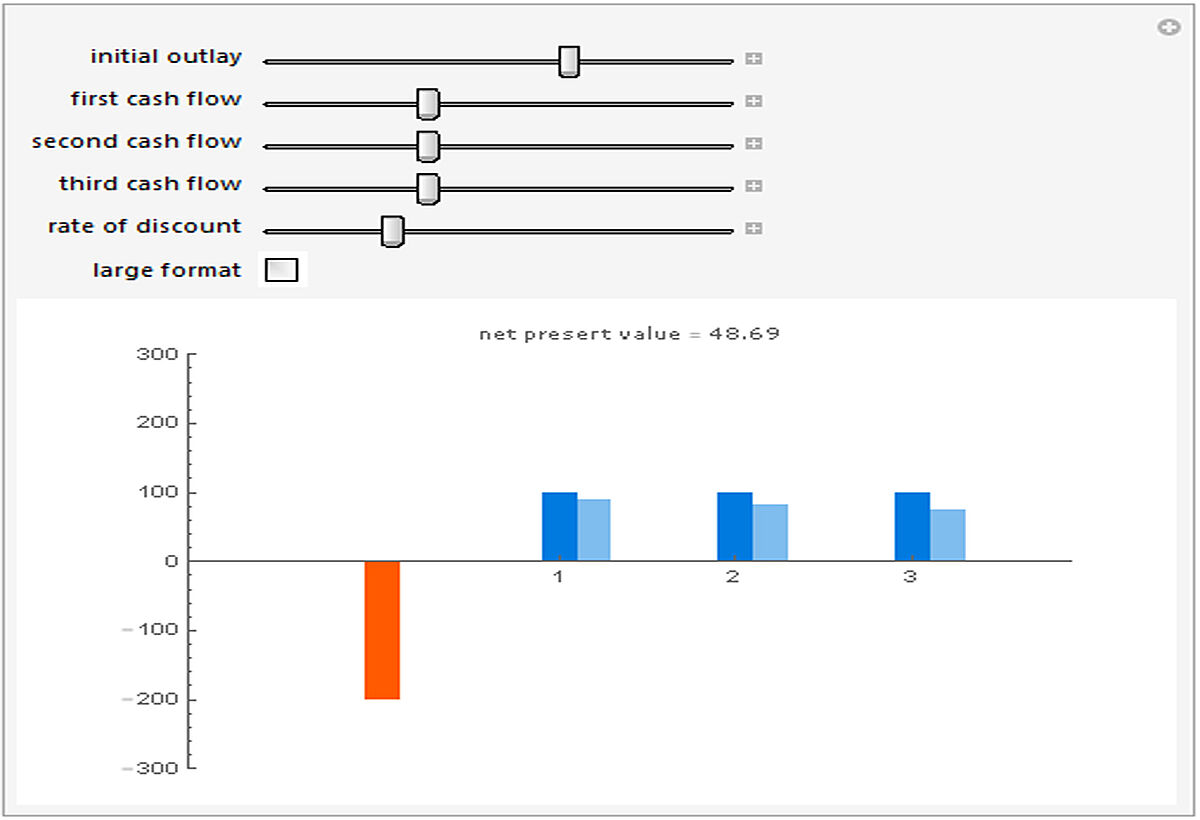

Net Present Value

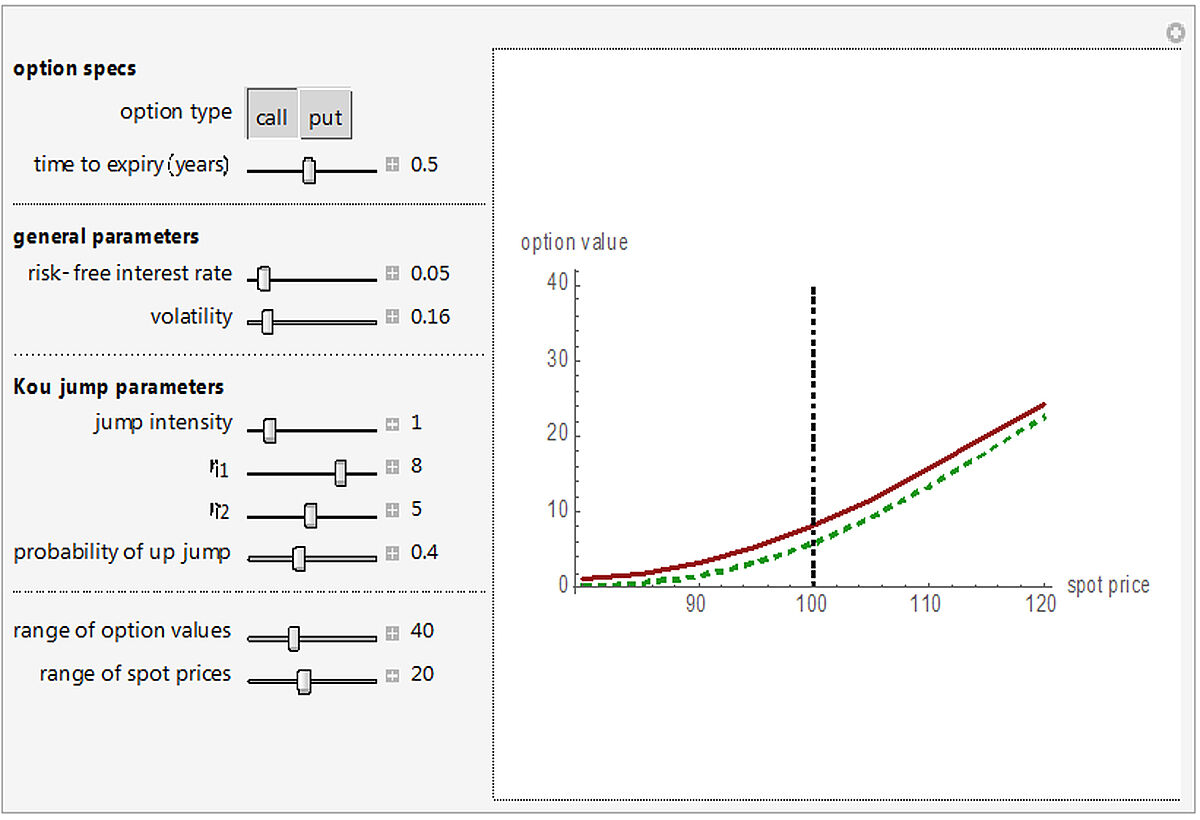

Option Prices in the Kou Jump Diffusion Model

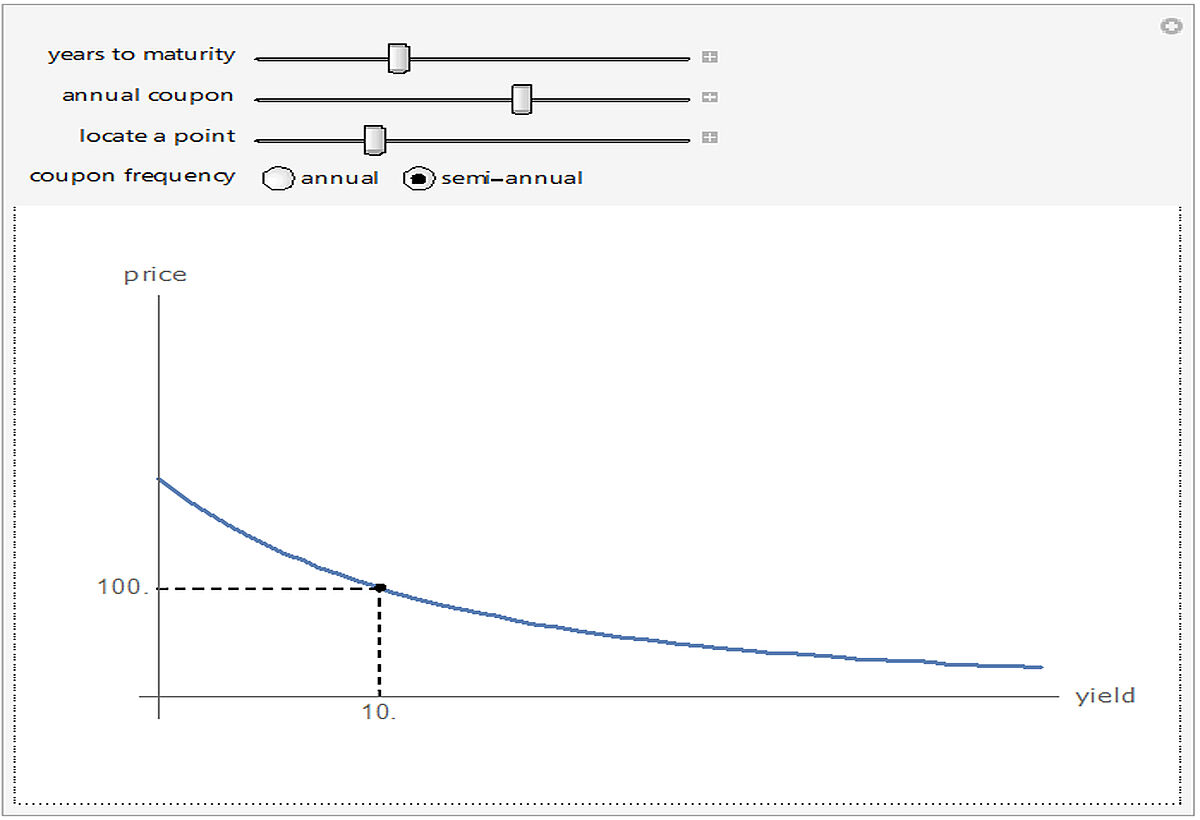

Price-Yield-Curve

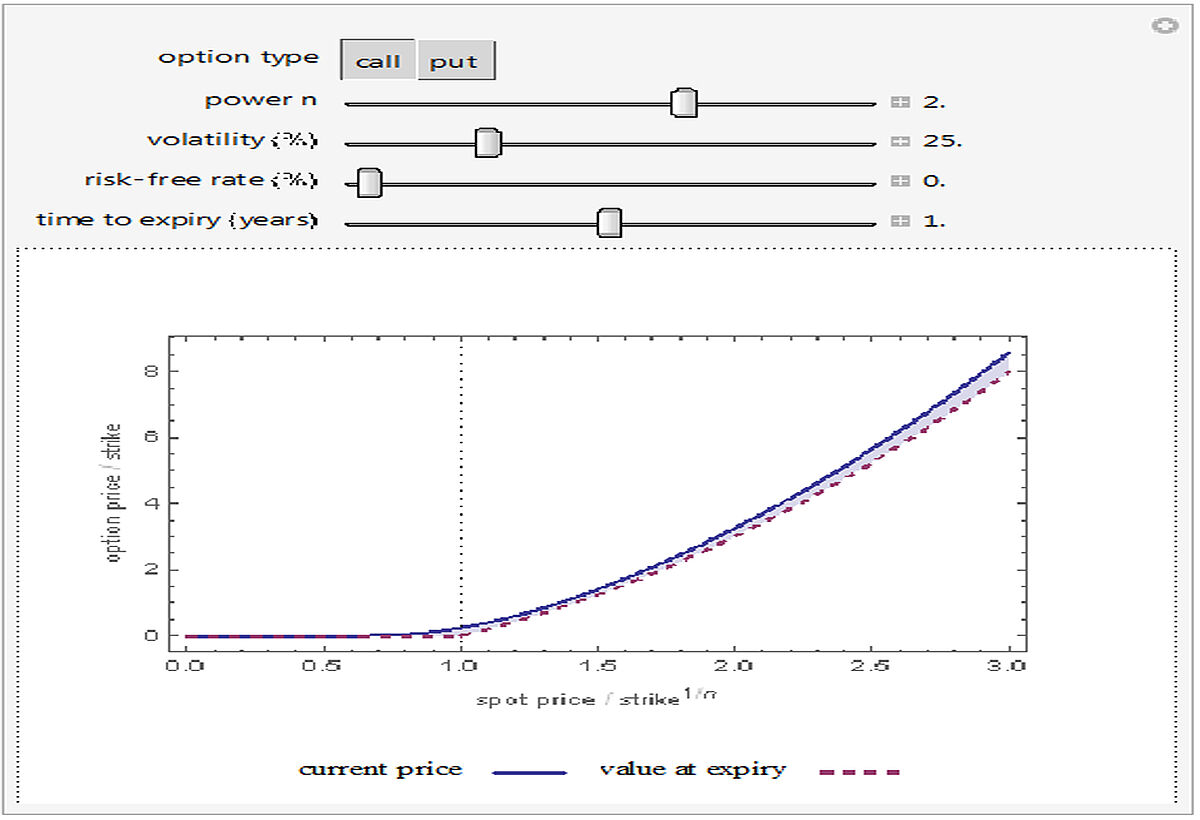

Pricing Power Options in the Black Scholes Model

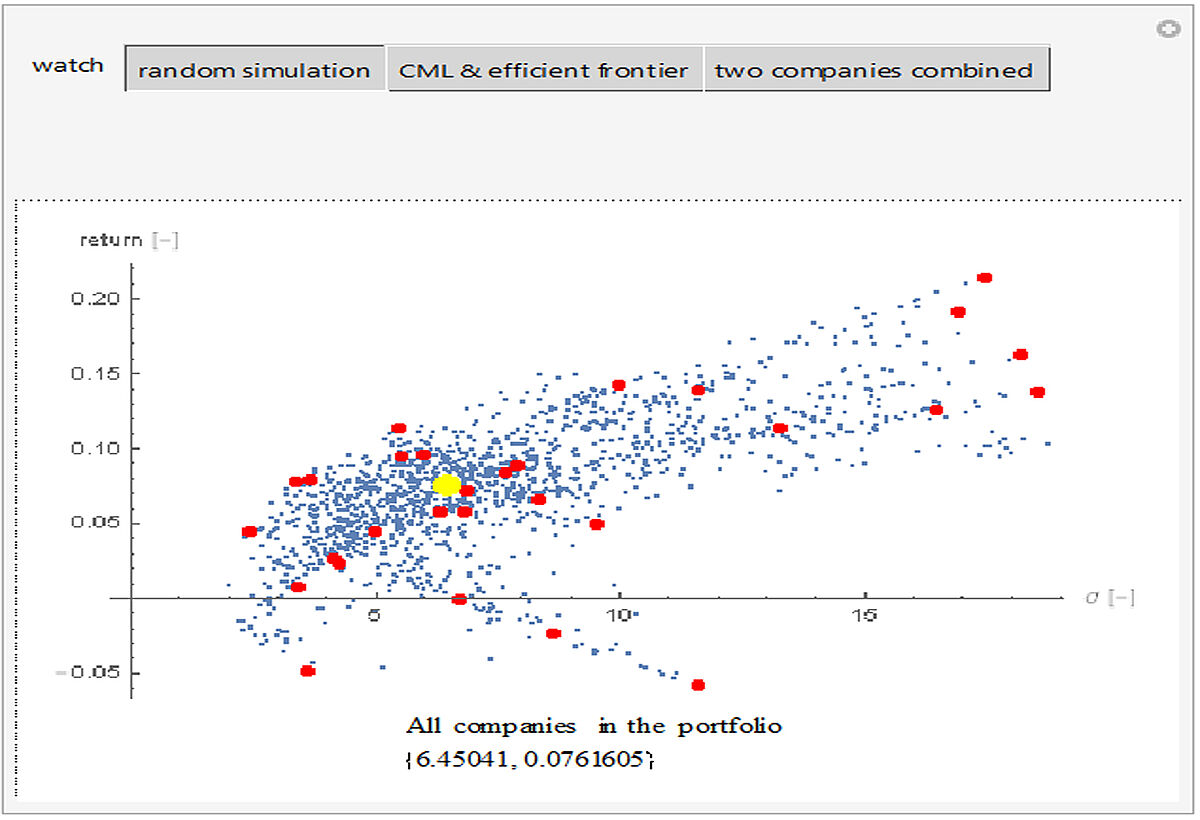

Random Simulation of a Financial Portfolio

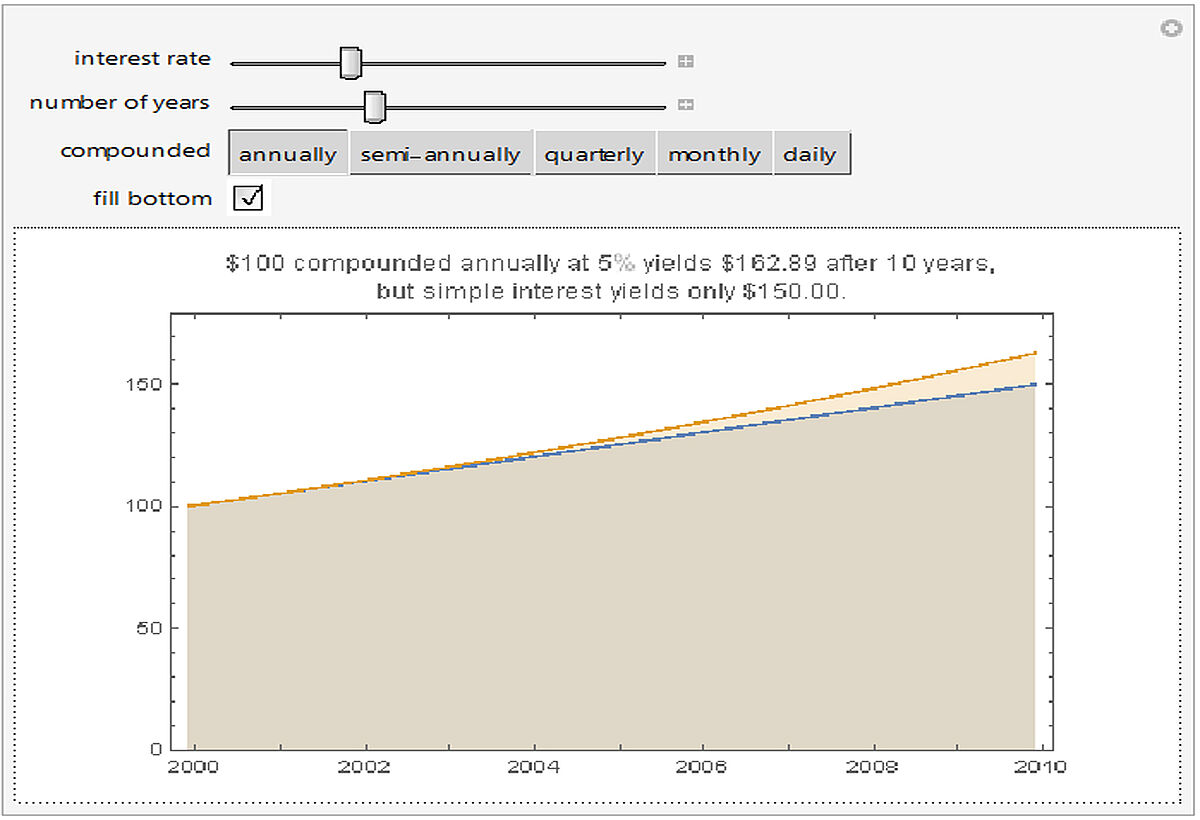

Simple versus Compound Interest

Term Structure of Interest Rates

The Itô Integral and Itô's Lemma

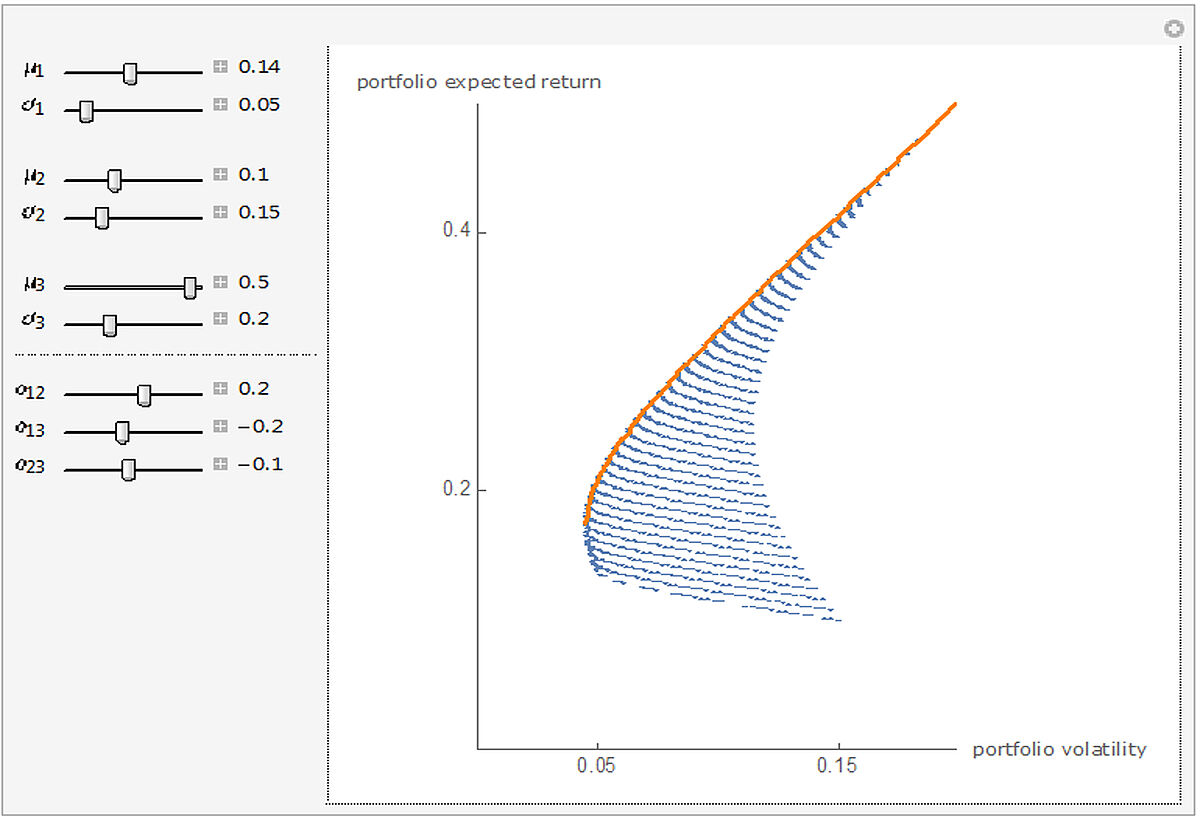

Three Asset Efficient Frontier

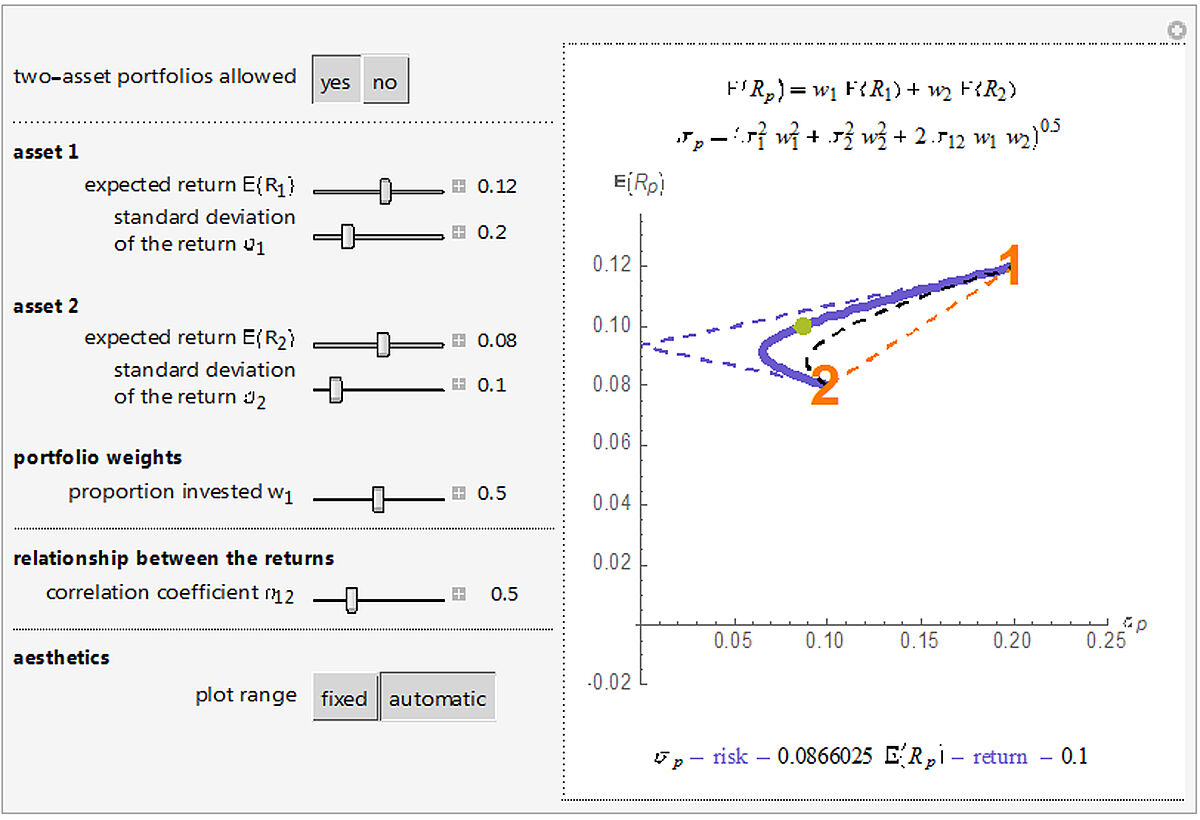

Two Asset Markowitz Feasible Set

Volatility Surface in the Heston Model

Yield Spot and Forward Curves

Nach oben